WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

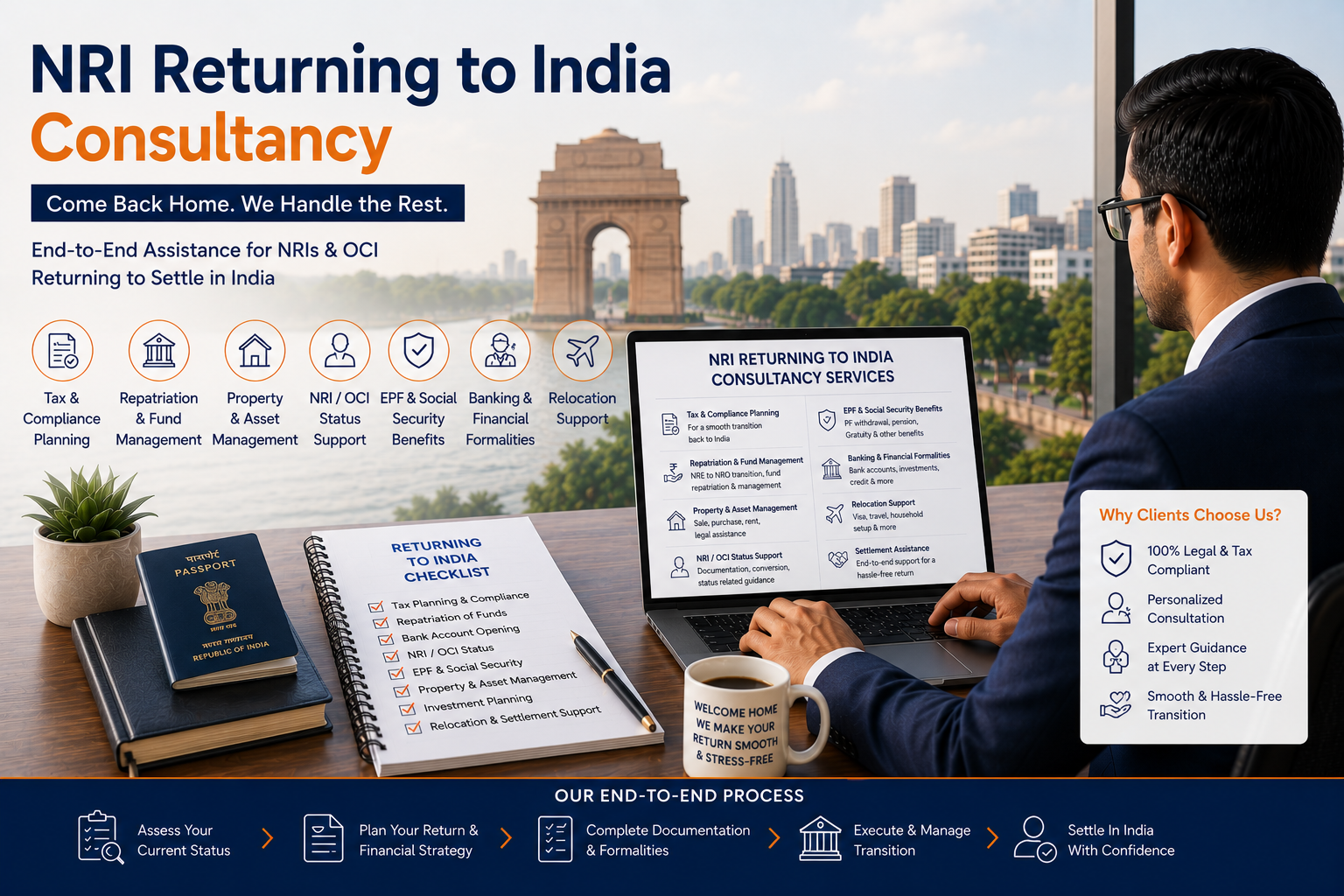

Returning to India after living overseas is not simply a relocation decision. For an NRI, OCI Card Holder, Green Card Holder, H-1B professional, UK resident, Canadian PR, UAE resident, global executive, entrepreneur, investor, or family returning from abroad, the timing and structure of the move can significantly affect Indian tax residency, RNOR eligibility, taxation of foreign income, foreign investments, retirement accounts, bank accounts, FEMA compliance, DTAA relief, and long-term wealth planning.

At Dinesh Aarjav & Associates, we provide end-to-end Returning to India consultancy for NRIs and overseas Indians relocating from the USA, Canada, UK, UAE, Singapore, Australia, New Zealand, Europe, and other global jurisdictions. Our advisory covers return-date planning, RNOR strategy, foreign asset review, NRE/NRO/FCNR/RFC account transitions, US 401(k) and IRA planning, UK pension and Canadian RRSP review, DTAA analysis, foreign tax credits, FEMA compliance, and post-return Indian tax filing.

With more than 25 years of professional experience and a cross-border team of Chartered Accountants, CPAs, EAs, and ACCAs, we help returning Indians make the move to India tax-efficient, compliant, and financially well planned.

If you are returning to India from the USA, UK, Canada, UAE, Singapore, Australia, or Europe, your return date, Indian tax residency, RNOR eligibility, foreign investments, retirement accounts, bank accounts, and FEMA status should be reviewed before you relocate.

A structured Returning to India tax plan can help you:

This planning is especially important for returning NRIs with global investments, stock compensation, overseas retirement accounts, Indian property, business interests, or income in more than one country.

We regularly advise:

A US CPA may understand US tax filings. A UK accountant may understand HMRC reporting. A local Indian tax preparer may understand an Indian income-tax return. However, the most valuable Returning to India decisions often sit between jurisdictions.

These decisions include:

Our Returning to India advisory is designed as a coordinated roadmap covering the period before relocation, the year of return, the RNOR phase, and the transition to full Indian residency.

Your Returning to India Tax Planning Timeline

| Phase | When | Primary Planning Focus |

| Phase 1: Before You Move | 6–24 months before return | Return date, residency projection, foreign assets, retirement accounts, property, DTAA, and investment-sale timing |

| Phase 2: Year of Return | Financial year in which you move | NRI/RNOR/ROR status, income allocation, bank-account redesignation, foreign tax credits, and documentation |

| Phase 3: RNOR Transition Window | Eligible post-return years | Foreign income, overseas investments, retirement-account distributions, reporting, and tax-efficient restructuring |

| Phase 4: Full Indian Residency | After RNOR ends | Global-income planning, foreign-asset reporting, long-term portfolio, estate, and succession planning |

Your Indian tax position after returning depends primarily on your residential status for each financial year. The principal categories are:

An NRI is generally taxed in India on Indian-source income and income received in India, subject to applicable law. An RNOR may provide a valuable transition period in which certain foreign income may receive different tax treatment, depending on the nature, source, receipt and connection of that income. An ROR is generally taxable in India on global income and may have wider foreign-asset reporting obligations.

A return-date review should be completed before relocation. A few days can materially affect tax residency, particularly around the April-to-March Indian financial year.

| Status | Broad Tax-Planning Relevance |

|---|---|

| NRI | Indian income and India-linked income are generally the primary focus. |

| RNOR | Transitional phase; certain foreign income may receive favourable treatment, subject to facts and applicable law. |

| ROR | Global income and broader foreign-asset reporting obligations may become relevant. |

RNOR, or Resident but Not Ordinarily Resident, is one of the most important tax-planning concepts for NRIs returning to India. It can provide a valuable transition period between non-resident status and full Indian taxation on global income, making advance planning essential before relocation.

RNOR eligibility depends on travel history, residential status in earlier financial years, the number of days spent in India and other applicable conditions under the Income-tax Act. It should never be assumed merely because a person has returned from abroad. A detailed residential-status calculation is necessary to determine eligibility.

For eligible returning Indians, RNOR planning may be relevant for:

RNOR is not a blanket exemption from tax. The tax treatment depends on the nature of the income, where it arises, where it is received, its connection with India and the individual's overall facts and circumstances. Professional tax planning can help maximize available benefits while ensuring full compliance with Indian tax laws.

Eligibility for RNOR status must be assessed based on the statutory residential-status provisions under the Income-tax Act and the individual's historical stay in India. A customized residential-status calculation should always be completed before finalizing the return date, as even a small change in the timing of relocation may affect tax residency and the availability of RNOR benefits.

The duration of RNOR status depends on the individual's residential history and satisfaction of the applicable statutory conditions under the Income-tax Act. Since eligibility must be evaluated for each financial year, the position should be reviewed annually to ensure continued compliance and effective tax planning.

Certain categories of foreign income may receive different tax treatment during the RNOR period. However, the taxability depends on the nature of the income, where it accrues or arises, where it is received, its connection with India and the applicable legal provisions. Foreign salary, business income, investment income, pension income, rental income and capital gains should each be reviewed separately before determining their tax treatment.

Once an individual becomes a Resident and Ordinarily Resident (ROR), Indian taxation generally extends to global income, and foreign asset and income reporting obligations may become significantly broader. Accordingly, tax planning should continue beyond the RNOR period to ensure efficient investment structuring, proper foreign tax credit planning, ongoing FEMA compliance and timely fulfillment of annual reporting obligations.

A successful return-to-India strategy begins long before the actual relocation. Proper planning before the return date can help optimize residential status, minimize tax liabilities, preserve available treaty benefits and ensure a smooth transition from non-resident to resident tax status.

India follows an April-to-March financial year for income-tax purposes. The month and date of return can significantly influence residential status, RNOR eligibility and the timing of Indian tax exposure. A carefully planned return date may create valuable tax-planning opportunities.

Review the timing of foreign salary, annual bonuses, deferred compensation, consulting income, severance payments and final employment settlements before and after relocation to determine the most tax-efficient approach and avoid unintended tax consequences.

Equity compensation requires careful cross-border tax planning. Review the vesting, exercise and sale of RSUs, ESOPs, ESPPs and stock options, together with withholding taxes, income sourcing, foreign tax credit availability and reporting obligations in both jurisdictions.

Evaluate the timing of planned sales of foreign shares, ETFs, mutual funds, private-company holdings, overseas real estate and Indian investments before any change in residential status. Proper planning can significantly improve overall tax efficiency.

Analyse applicable Double Taxation Avoidance Agreement (DTAA) provisions, Tax Residency Certificate (TRC) requirements, foreign taxes paid, Form 67 documentation and foreign tax credit eligibility to minimize the risk of double taxation and maximize available treaty benefits.

Review retirement accounts such as US 401(k), Traditional IRA, Roth IRA, UK pension schemes, Canadian RRSPs, CPF, Australian superannuation and other retirement arrangements before making withdrawals, rollovers or distributions. Advance planning can help optimize taxation and preserve long-term retirement benefits.

Banking transitions are among the first practical steps after returning to India. NRE and NRO accounts, FCNR deposits, resident accounts and RFC accounts each serve different purposes and are subject to different tax treatment and FEMA regulations. A timely review of banking arrangements can help ensure regulatory compliance, preserve foreign currency holdings where permitted and facilitate efficient financial management after relocation.

Once an individual becomes a resident in India under FEMA, NRE accounts should be reviewed for re-designation or conversion in accordance with applicable regulations. Proper planning helps avoid compliance issues and ensures that banking arrangements remain aligned with the individual's residential status.

Review the status of NRO accounts, including income credits, rental receipts, remittance requirements, tax deductions and supporting documentation. Appropriate account management can simplify ongoing financial transactions and regulatory compliance.

FCNR deposits should be reviewed with reference to their maturity dates, continued eligibility and available conversion options following any change in residential status. Advance planning helps optimize both banking and tax outcomes.

Eligible returning Indians may consider opening a Resident Foreign Currency (RFC) account to continue holding eligible foreign currency assets in accordance with FEMA regulations. The suitability of an RFC account depends on individual circumstances and long-term financial objectives.

A strategic review should be undertaken to determine whether overseas funds should remain outside India, be repatriated to India or be maintained through permitted banking structures. This decision should consider tax implications, future investment plans, liquidity requirements and FEMA compliance.

A banking strategy should always be coordinated with overall tax planning rather than treated as a separate administrative task. Integrating banking decisions with residential-status planning, DTAA considerations, foreign tax credits and long-term investment objectives can help ensure a smooth and tax-efficient transition back to India.

| Asset or Account | Questions to Review Before Return |

|---|---|

| US 401(k), Traditional IRA or Roth IRA | Should the account be retained, withdrawn or rolled over? Review distribution timing, Indian tax implications, DTAA provisions and reporting obligations. |

| UK Pension | Review withdrawal strategy, annuity options, income timing, India–UK DTAA implications and supporting documentation. |

| Canadian RRSP / TFSA | Evaluate withdrawal timing, Canadian and Indian tax implications, foreign tax credit availability and reporting requirements. |

| Foreign Shares & ETFs | Assess whether to hold or sell, capital gains implications, dividend taxation, reporting obligations and future liquidity needs. |

| RSUs, ESPPs & ESOPs | Review vesting schedules, exercise timing, sale strategy, withholding taxes, income sourcing and foreign tax credit implications. |

| Foreign Property | Evaluate rental income, sale planning, capital gains taxation, taxes paid overseas and remittance strategy. |

| Foreign Bank Accounts | Review whether accounts should be retained, required documentation, FEMA implications and future reporting obligations. |

| Foreign Mutual Funds / Insurance Products | Assess tax classification, income recognition, liquidity considerations and ongoing reporting requirements. |

| Private Company or Startup Shares | Review valuation, liquidity event planning, tax residency implications and potential capital gains consequences. |

Returning to India does not automatically mean that every foreign asset must be sold. However, each asset should be reviewed from the perspectives of Indian taxation, FEMA regulations, reporting obligations, liquidity requirements and long-term wealth planning. A structured review before returning can help optimize tax efficiency and avoid unnecessary compliance issues.

Our advisory covers:

A person's income-tax residential status and FEMA residential status are closely related but governed by different legal provisions. Returning Indians should review both before making banking, investment, remittance or property-related decisions to ensure complete regulatory compliance.

Our FEMA advisory covers:

Early FEMA planning can reduce delays with banks and financial institutions, prevent incorrect account usage or investment treatment after returning to India and ensure that cross-border assets and financial transactions remain fully compliant with applicable regulations.

Returning from the United States requires careful coordination between Indian and US tax laws. Decisions made before relocating can significantly affect tax residency, foreign tax credits, retirement accounts, investment taxation and ongoing compliance in both countries. Our advisors assist H-1B and L-1 visa holders, Green Card holders, US citizens of Indian origin, executives, entrepreneurs and families with comprehensive India-US tax planning before and after their return to India.

Our advisory includes:

Our objective is to help returning NRIs achieve a smooth transition to India while optimizing tax efficiency, preserving treaty benefits, maintaining compliance in both jurisdictions and protecting long-term wealth through coordinated India-US tax planning.

Returning to India from Canada requires coordinated planning under both Indian and Canadian tax laws. Decisions regarding tax residency, registered retirement accounts, investments, property holdings and foreign tax credits should ideally be made before relocation to minimize tax exposure and ensure seamless compliance in both jurisdictions. Our advisory services assist Canadian-based NRIs with comprehensive cross-border tax planning before and after their return to India.

Our advisory includes:

Our objective is to help returning NRIs from Canada achieve a smooth transition to India through effective residential-status planning, optimized foreign tax credit utilization, coordinated India-Canada DTAA advisory and long-term cross-border tax compliance.

Returning to India from the United Kingdom requires coordinated planning under both Indian and UK tax laws. Careful review of UK tax residency, pension benefits, investment portfolios, property holdings and treaty provisions before relocation can significantly improve tax efficiency and reduce future compliance risks. Our advisory services help returning Indians navigate cross-border tax obligations while ensuring a smooth financial transition to India.

Our advisory includes:

Our objective is to help returning Indians from the UK optimize India-UK tax planning, preserve available treaty benefits, manage overseas assets efficiently and maintain full compliance with both Indian and UK tax regulations throughout the transition.

Returning to India from the United Arab Emirates requires careful planning of tax residency, banking arrangements, investments and cross-border financial affairs. Although the UAE does not levy personal income tax in most situations, returning residents should review the India-UAE DTAA, FEMA regulations, foreign assets and the timing of their return to ensure a smooth and tax-efficient transition.

Our advisory includes:

Our objective is to help returning residents from the UAE structure their financial affairs efficiently, optimize available DTAA benefits, ensure FEMA and banking compliance, protect overseas assets and achieve a seamless transition to Indian tax residency.

Returning to India from Singapore requires careful planning of tax residency, retirement savings, investments and cross-border tax obligations. Professionals, executives and investors should review CPF balances, investment portfolios, equity compensation and banking arrangements before relocating to optimize tax outcomes and ensure compliance with both Indian and Singaporean regulations.

Our advisory includes:

Our objective is to help returning Indians from Singapore achieve a seamless financial transition through effective tax planning, optimized DTAA benefits, efficient management of overseas investments and retirement assets, and full compliance with Indian tax and FEMA regulations.

Returning to India from Australia or New Zealand requires careful coordination of tax residency, retirement savings, foreign investments and cross-border tax obligations. Individuals should review superannuation or other retirement arrangements, investment portfolios, property holdings, capital gains and foreign tax credit availability before relocating to ensure a tax-efficient transition and continued compliance with applicable laws.

Our advisory includes:

Our objective is to help returning Indians from Australia and New Zealand optimize cross-border tax planning, preserve available treaty benefits, efficiently manage overseas assets and retirement savings, and ensure full compliance with Indian tax and FEMA regulations after returning to India.

Returning to India from Germany, the Netherlands, France, Ireland, Switzerland, Luxembourg or other European countries requires careful cross-border tax planning. Tax residency, pension arrangements, foreign investments, property holdings, foreign tax credits and DTAA benefits should be reviewed before relocation to ensure a smooth transition and long-term tax efficiency. Our advisory helps returning Indians manage both Indian and European tax obligations while remaining compliant with applicable tax and FEMA regulations.

Our advisory includes:

Our objective is to help returning Indians from Europe optimize cross-border tax planning, maximize treaty benefits, efficiently manage overseas assets and pensions, and ensure seamless compliance with Indian tax laws, FEMA regulations and applicable international tax requirements.

Before returning to India, it is advisable to retain both digital and physical copies of all important financial, tax, banking and immigration documents. Proper documentation can simplify tax compliance, support foreign tax credit claims, facilitate banking transitions and help resolve future queries from tax authorities or financial institutions.

Before returning, retain digital and physical copies of:

Even a difference of a few days can change your residential status, RNOR eligibility and the timing of Indian tax liability. Return-date planning should be completed before relocation.

Many returning NRIs review their foreign income and overseas assets only after becoming Indian residents. Early RNOR planning can help optimize tax efficiency during the transition period.

NRE accounts should be reviewed and re-designated where required after a change in FEMA residential status. Delays may result in regulatory and banking compliance issues.

Foreign taxes paid are sometimes not properly documented or claimed, resulting in avoidable double taxation and loss of available treaty benefits.

Overseas brokerage accounts, pension plans, rental properties, bank accounts and other foreign investments should be reviewed before returning to assess their Indian tax and reporting implications.

Decisions relating to foreign shares, ETFs, mutual funds, real estate, retirement accounts and other investments should be evaluated from both Indian and overseas tax perspectives before any transaction is undertaken.

Compliance with income-tax laws does not automatically ensure compliance with FEMA regulations. Both should be reviewed together when planning a return to India.

Post-return tasks such as KYC updates, bank account re-designation, income-tax filing, foreign tax credit claims and regulatory reporting should be completed promptly to avoid unnecessary compliance issues.

A return to India is a rare tax-planning opportunity. Decisions made before becoming an Indian resident can significantly influence your tax exposure, foreign asset position, banking arrangements, FEMA compliance and long-term wealth strategy for years to come. Careful planning before relocation can help optimize tax efficiency, preserve available treaty benefits and ensure a smooth financial transition.

For personalized Returning to India Tax Planning, RNOR advisory, FEMA support, DTAA analysis, RFC account planning, foreign investment review and post-return tax compliance, contact Dinesh Aarjav & Associates.

A person who is not a resident of India is considered a Non-Resident of India (NRI). You are a resident if your stay in India for a given financial year is: 182 days or more 60 days or more and 365 days or more in the 4 immediately preceding previous years. In case one does not satisfy either of the above conditions, one will be considered an NRI.

An NRI, like any other individual taxpayer, must file return of income in India if gross total income received in India exceeds Rs 2.5 lakh for any given financial year. Further, the due date for filing a return for an NRI is also 31 July of the assessment year or extended by the Government.

If there is a rental income in India, then Income tax return needs to be filed in India mentioning the PAN and tax to be paid. Also to note, that though holding one property in India is considered as ‘self-owned’, a second property, even if it is not on rent, is considered ‘deemed rented’ and tax needs to be paid for that. One can, however, show 30% of the deemed rental as ‘maintenance cost’. There is no tax to be paid abroad (say, USA) on ‘deemed’ income, but declaring it is important as during repatriation of funds from India, it should not cause any issue.

If an NRI receives income in India, such income is taxable in India, i.e. India as a source state has the right to tax such income. However, the country where such NRI is a resident will also have a right to tax such income as it is the residence state. This way, the NRI will end up getting taxed twice on the same income. To overcome this, India has entered into DTAAs with various countries. It will help eliminate double taxation by allowing the taxpayer to claim credit for foreign taxes paid while filing their return of income in the home country.

No, The Income tax Act applies to all persons who earn income in India. Whether they are resident or non-resident.

In case of resident individuals and companies, their global income is taxable in India. However non-residents have to pay tax only on the income earned in India or from a source/activity in India.

Yes, The dividend declared by Indian companies is taxable in the hands of the shareholders at the rate of 20.00% without providing for deduction under any provision of Income Tax Act.

You can authorize any person by way of a Power of Attorney to file your return. A copy of the Power of Attorney should be enclosed with the return.

Yes, if an NRI’s tax liability is expected to exceed Rs. 10,000 in a financial year, he must pay advance tax. Interest under Section 234B and Section 234C will be levied if advance tax is not paid.

You cannot maintain your NRE account and NRE FDs when you are an RNOR. You need to convert your NRE account to resident account immediately upon returning to India.

Open an RFC account. Resident Foreign Currency (RFC) is a Scheme approved by Reserve Bank of India permitting persons of Indian nationality or origin, who have returned to India on or after 18th April 1992 for permanent settlement (Returning Indians), after being resident outside India for a continuous period of not less than 1 year, to open foreign currency accounts with banks in India for holding funds brought by them to India.

Yes, of course, NRIs can buy life Insurance and health insurance in India and our term life rates in the country are among the best in the world. Therefore, there are a lot of NRIs who come and take a term plan here because the rates are attractive and we have the ability to give large value term life covers India has that ability to do that.

Yes, NRIs must close or re-designate their NRE accounts after moving back to India. According to the Foreign Exchange Management Act (FEMA), once you return to India with the intention of staying, you are considered a resident from that day forward. Therefore, your NRE account must be converted into a normal resident account, or closed, to comply with Indian regulations. Failing to do so within three months of your return can lead to penalties under FEMA.

If you are uncertain about your long-term plans and still hold a valid overseas visa, you are allowed to maintain your NRE and NRO accounts for a limited period. You can keep the accounts until you surpass the eligibility criteria of 120 to 183 days, depending on your situation. However, if you decide to stay in India, you must inform your bank and re-designate your accounts accordingly.

Interest earned on NRE accounts is tax-free only while you are a non-resident. Once you return to India, the interest on these accounts becomes taxable. To manage this, you can transfer your funds from the NRE account to a Resident Foreign Currency (RFC) account, which allows you to maintain your funds in foreign currency and enjoy repatriation benefits.

Upon returning to India, it is crucial to inform your bank, fund house, and insurance company about your change in residential status. As a resident Indian, your investments will now be subject to regular tax laws. Although there won’t be changes in tax laws for previous years, it’s important to update your status to avoid complications.

NRI-specific tax exemptions are no longer valid once you become a resident Indian. If you’ve made investments with tax benefits exclusive to NRIs, you will lose those benefits after becoming a resident. It’s essential to inform your investment house about your new status and consult with them regarding any potential tax implications.

The first step is to inform your bank about your change in residency status. The bank will guide you through the process, which may involve filling out a form or providing a written declaration. Your NRE account can be either re-designated as a resident savings account or converted to a Resident Foreign Currency (RFC) account. Each bank may have different procedures, so it’s advisable to consult with your bank directly for specific instructions.

The right date depends on your travel history, income, foreign assets, intended length of stay, and the Indian financial year. A return-date review should be completed before finalising relocation.

Eligible returning Indians may qualify for RNOR status. Eligibility depends on statutory conditions and residential history and should be calculated individually.

No. RNOR is not a blanket exemption. The treatment depends on the type, source, receipt, and connection of the foreign income with India.

Not automatically. Withdrawal, retention, rollover, and distribution timing should be reviewed through coordinated India-US tax planning before action is taken.

The Indian tax and reporting consequences should be reviewed before distributions or other transactions. The appropriate strategy depends on your facts, treaty position, and future plans.

In many cases, foreign shares and brokerage accounts can be retained, but Indian tax, FEMA, reporting, income, capital-gains, and future remittance implications should be reviewed.

You should inform the bank about the change in residential status and review re-designation, conversion, maturity, and RFC-account options.

Eligible returning Indians may be able to open an RFC account to hold foreign currency, subject to applicable rules and bank procedures.

Foreign tax credits may be available subject to applicable DTAA provisions, Indian tax rules, documentation, and filing requirements.

Disclosure requirements depend on residential status, the nature of assets, and applicable Indian tax rules. This should be reviewed annually.

A post-return review can still identify corrective actions for residential status, bank accounts, foreign tax credits, asset documentation, tax returns, and FEMA compliance.

For many cross-border situations, coordinated India and overseas advice is valuable. The appropriate support depends on citizenship, immigration status, income, assets, and continuing filing obligations.

FCA, B.Com (H)

FCA, ACCA, B. Com (H)

MBA (Int'l Banking & Finance), LLB, B. Com (H)

ACA, CISA, B. Com (H)

FCA, B.Com (H)

FCA, B.Com (H)

_standard.png)

CPA(USA), FCA, CISA, B.Com (H)

EA, CA, M.Com, B.Com (H)

CPA, FCA, B. Com (H)

CA, B.Com

FCA, B.Com (H)

FCA, ACCA, B. Com (H)

MBA (Int'l Banking & Finance), LLB, B. Com (H)

ACA, CISA, B. Com (H)

FCA, B.Com (H)

FCA, B.Com (H)

CPA(USA), FCA, CISA, B.Com (H)

EA, CA, M.Com, B.Com (H)

CPA, FCA, B. Com (H)

With over 21 years of experience, Mr. Abhishek Batra specializes in NRI taxation and cross-border corporate tax strategies. His expertise spans tax planning, compliance advisory, and financial structuring, helping individuals and businesses navigate complex international tax regulations.

Based in Canada, Mr. Batra offers tailored solutions to NRIs, expatriates, and global companies with operations in India. A Chartered Accountant, CPA, and SRCC graduate, he is known for delivering impactful financial strategies that support growth and compliance.

CA, B.Com

An Experienced Chartered Accountant with over 5 years of expertise in cross-border taxation, NRI taxation, and US tax compliances. She has extensive exposure in handling complex international tax matters, including India-US taxation, DTAA advisory, foreign disclosures, expatriate taxation, and tax planning for NRIs and returning Indians.

She is a Chartered Accountant and a Commerce Graduate, with strong proficiency in US tax filings and global tax advisory services.

.webp)