WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

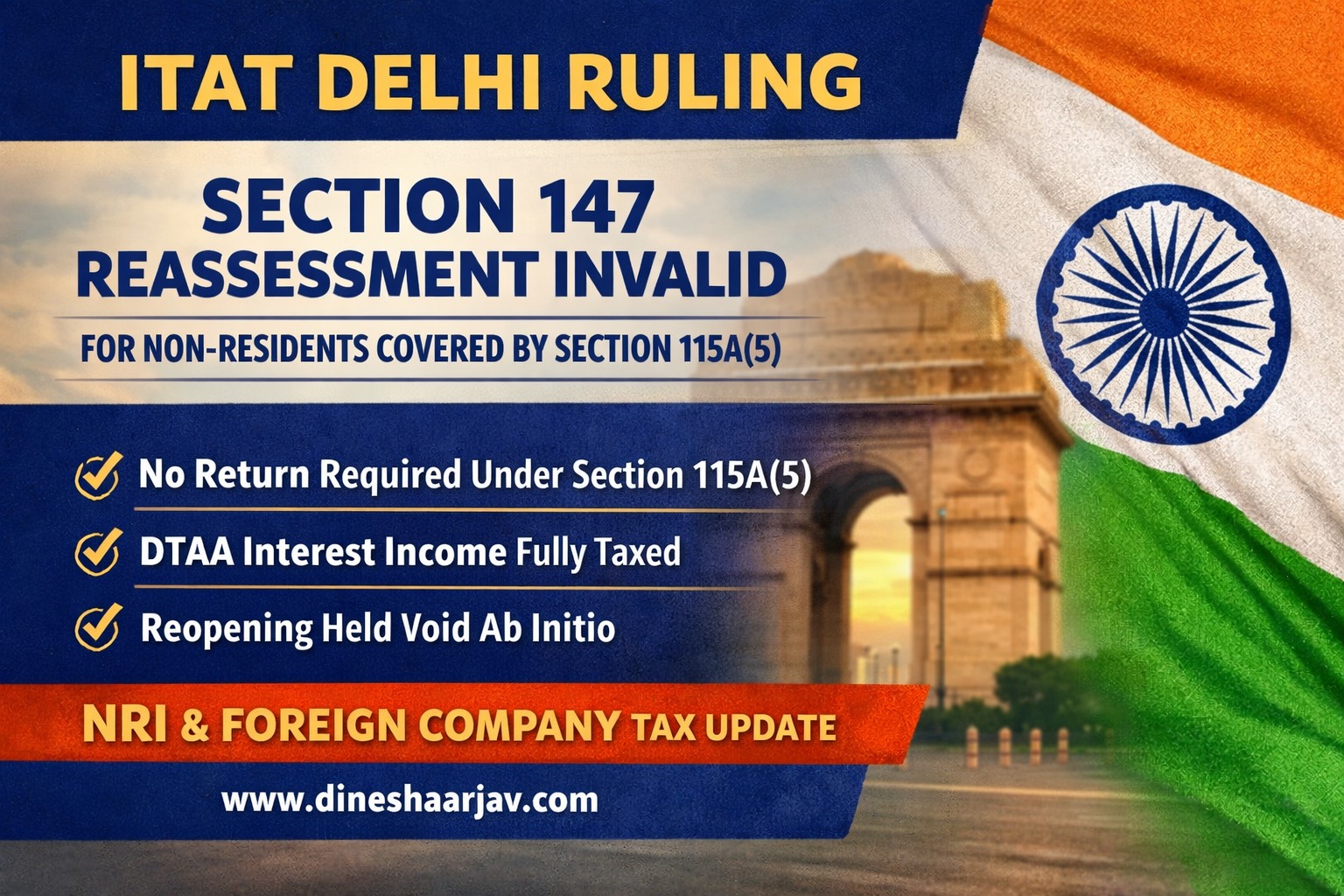

Section 115A(5) Return Filing Exemption for Non-Residents – Confirmed by ITAT Delhi

In a landmark ruling strengthening non-resident tax compliance protection in India, the Delhi Bench of the Income Tax Appellate Tribunal (ITAT) has held that reassessment proceedings under Section 147 cannot be initiated solely because a non-resident did not file an income tax return in India, where Section 115A(5) specifically removes the return filing obligation.

The decision in Kisan International Trading FZE vs ACIT (ITA No. 6152/Del/2024) provides decisive clarity for:

The assessee was a UAE tax-resident foreign company receiving interest income from an Indian borrower (IFFCO).

Key facts:

Since the only Indian income was interest subject to DTAA withholding tax, the assessee invoked Section 115A(5), which states that no Indian income tax return is required when correct TDS is deducted on interest or dividend income of non-residents.

Despite clear compliance:

The AO alleged income escaping assessment solely due to non-filing of return, without examining:

Worse, the AO incorrectly doubled the income and passed an erroneous reassessment order.

The ITAT categorically held:

Where:

Filing an Indian income tax return is not required

Non-filing cannot be treated as income escaping assessment

Reassessment triggered merely by the automated Non-Filer Monitoring System was held to be:

The Tribunal reaffirmed:

The ITAT relied on:

Both judgments confirm:

The Tribunal ruled:

This judgment is a major relief for:

At Dinesh Aarjav & Associates, we advise:

With 25+ years of NRI and international tax experience, we help overseas clients stay compliant and protected through effective NRI tax planning.

Breaking NRI Tax Update: ITAT Delhi Cancels Penalty on NRI Because Income Tax Notice Was Never Served

Foreign Tax Credit for NRIs and RNORs: ITAT Delhi’s Landmark Ruling in Aditya Khanna vs ITO

ITAT Chennai Ruling on NRI Residential Status: Overseas Income Not Taxable in India for Non-Residents

ITAT Mumbai’s Landmark Ruling: Section 69 Cannot Override Section 5(2)

CA Dinesh K. Jain is the Founder and Mentor of Dinesh Aarjav & Associates, with over 35 years of experience in NRI taxation, cross-border advisory, project financing, and tax litigation. He has guided numerous NRIs and global families through complex tax and regulatory matters involving investments, repatriation, and international financial planning.

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)