WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

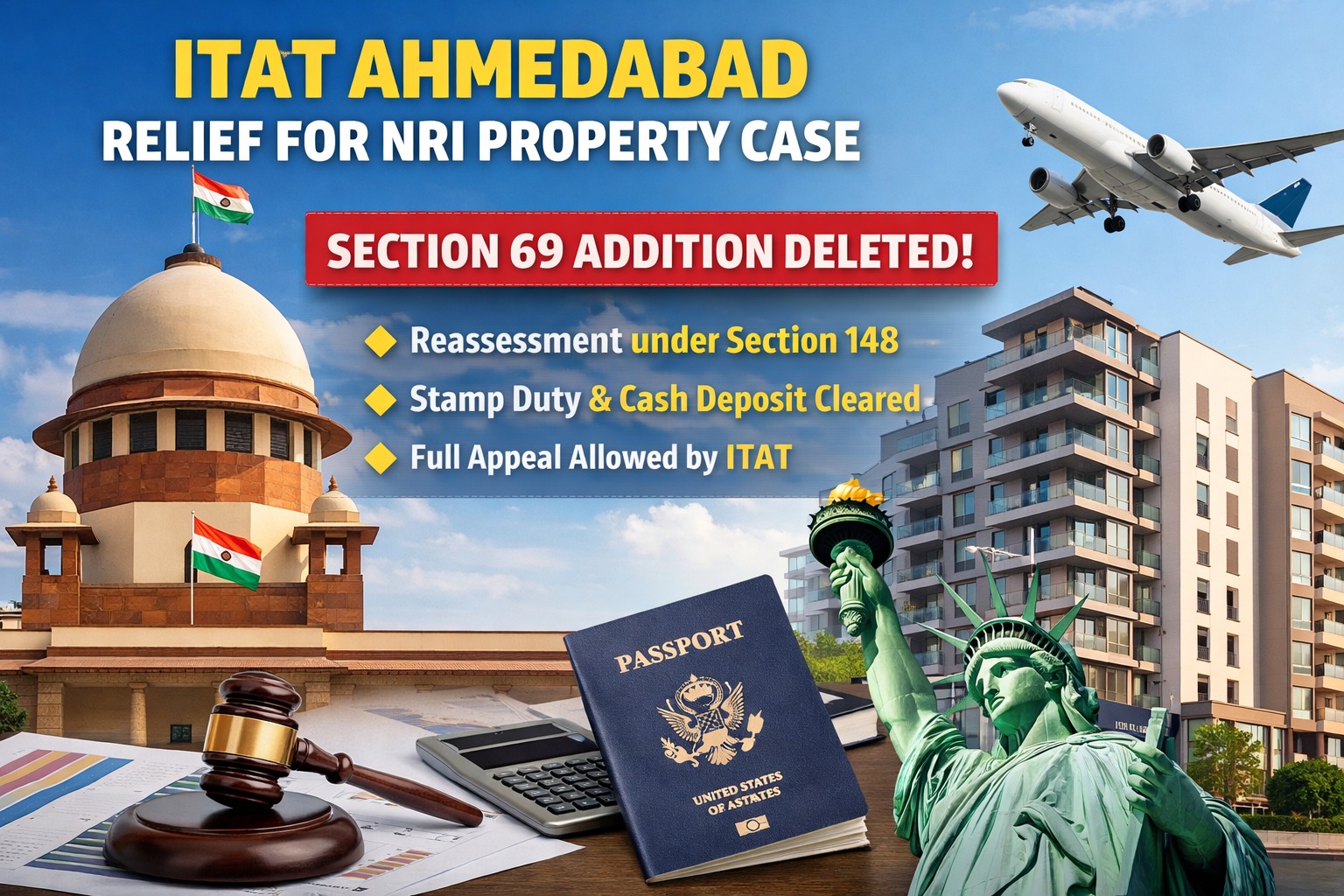

In a significant ruling for Non-Resident Indians (NRIs), the Income Tax Appellate Tribunal (ITAT), Ahmedabad Bench granted complete relief to a US-based NRI in a case involving Section 69 unexplained investment, reassessment under Section 148, and NRI property purchase in India

This judgment is highly relevant for NRIs facing:

If you are an NRI investing in Indian real estate, this case provides critical guidance on documentation, compliance, tax planning, and NRI investment in India tax defense strategy.

The assessee:

Since no original Income Tax Return (ITR) was filed for AY 2016-17, the Income Tax Department issued a notice under Section 148 initiating reassessment proceedings.

The Assessing Officer passed an order under:

Proposing an addition of ₹57,24,172 as unexplained investment under Section 69.

The matter went before the Dispute Resolution Panel (DRP).

The DRP:

The assessee appealed before ITAT Ahmedabad.

The Assessing Officer treated the cash deposit in the bank account as unexplained investment under Section 69.

Assessee’s Defense:

ITAT Ruling:

The Tribunal held that:

Addition of ₹1,00,000 deleted

The department treated:

As unexplained investment under Section 69.

Evidence Submitted:

ITAT Decision:

The Tribunal observed that:

Entire addition of ₹4,32,280 deleted

The ITAT Ahmedabad allowed the appeal in full and deleted the entire addition of ₹5,32,280 made under Section 69.

This ruling reinforces that:

Proper banking trail + documentary evidence = Strong defense in NRI reassessment cases.

This case answers critical tax queries frequently searched online:

Can NRIs receive notice under Section 148?

Yes. Failure to file ITR or mismatch in financial transactions can trigger reassessment.

Can stamp duty be treated as unexplained investment?

Yes, if proper documentation is not maintained.

Are cash deposits in NRE/NRO accounts taxable?

Not automatically. However, unexplained deposits can attract Section 69 addition.

How to defend unexplained investment addition?

Maintain:

Always File Your Income Tax Return (ITR)

Even if no taxable income arises, filing prevents future reassessment issues.

Maintain Complete Fund Trail

Especially for:

Respond Properly to Section 148 Notice

A technical and well-documented reply can prevent large additions.

Seek Professional Representation in DRP & ITAT

Improper handling at draft assessment stage can lead to prolonged litigation.

At Dinesh Aarjav & Associates, we specialize in:

With over 25+ years of experience in NRI taxation and cross-border advisory, we provide structured, documentation-backed defense in complex tax matters.

This ITAT Ahmedabad ruling provides major relief for NRIs facing additions under Section 69 for property transactions, including issues arising during sale of property by NRI cases.

The decision clearly establishes:

If you are an NRI who has received:

Early professional advice can significantly improve your outcome.

CA Dinesh K. Jain is the Founder and Mentor of Dinesh Aarjav & Associates, with over 35 years of experience in NRI taxation, cross-border advisory, project financing, and tax litigation. He has guided numerous NRIs and global families through complex tax and regulatory matters involving investments, repatriation, and international financial planning.

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)