WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

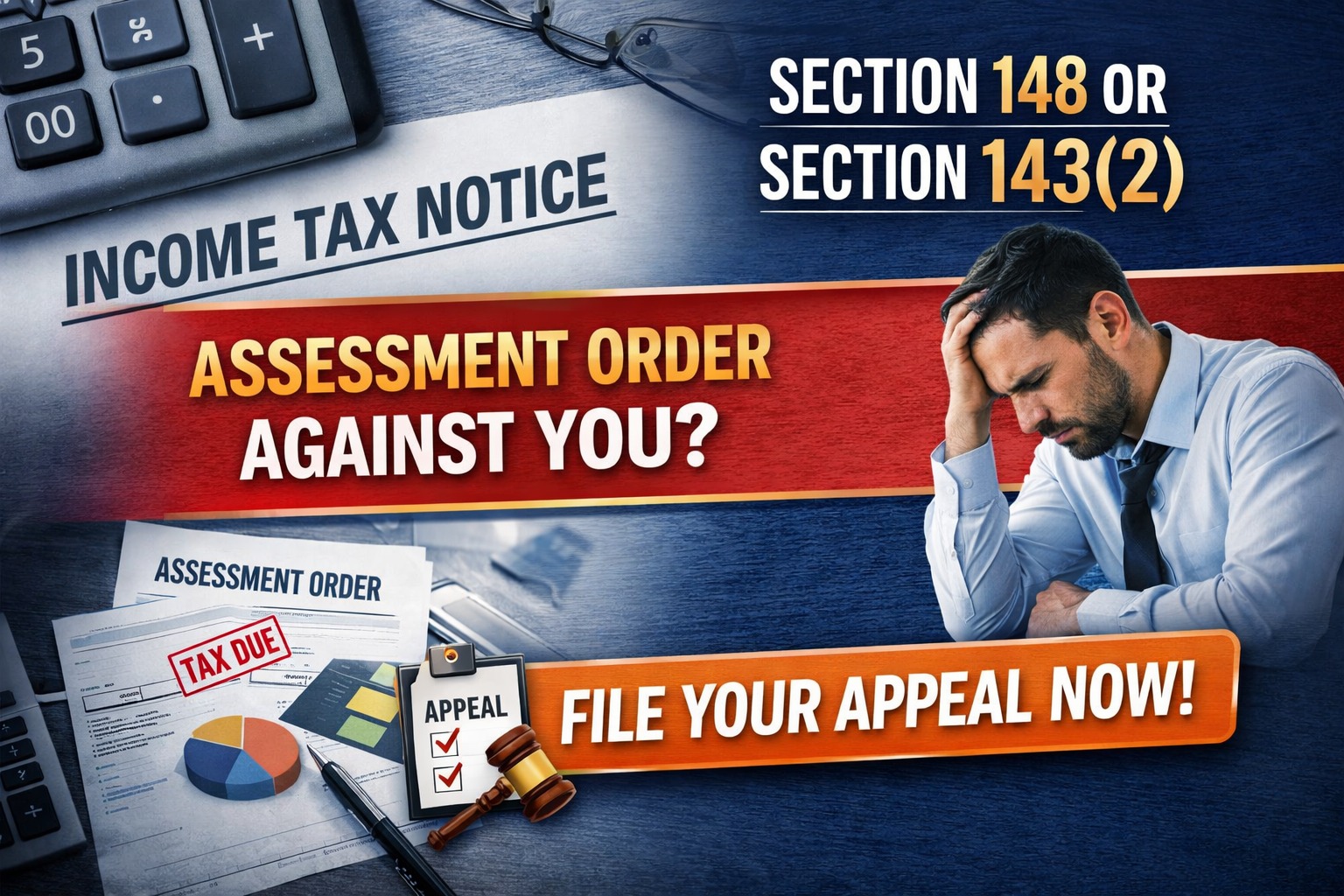

In the recent assessment cycle, many taxpayers, especially Non-Resident Indians (NRIs), have received Income Tax communications under Sections 131(1A), 148 and 143(2).

While Section 131(1A) is a summons for inquiry and information gathering, the actual assessment orders are typically passed under Section 147 (pursuant to Section 148) or Section 143(3) (pursuant to Section 143(2)).

A growing number of taxpayers are facing situations where:

If your Income Tax assessment is not in your favour despite compliance, you still have strong legal remedies available under the Income Tax Act, 1961.

It is important to distinguish between different types of Income Tax notices:

Assessment orders are generally passed under:

Even after filing responses, taxpayers often receive adverse orders due to:

This leads to unjustified tax demands, interest, and penalties.

If an assessment order has been passed under Section 147 or 143(3), the primary remedy is:

Filing an Appeal under Section 246A

Before the Commissioner of Income Tax (Appeals)

Key Features:

This is the most effective way to contest an incorrect assessment order.

If the 30-day timeline has lapsed, an appeal can still be filed with a Condonation of Delay Petition.

Valid grounds include:

Authorities generally allow condonation where reasonable cause is demonstrated.

A major advantage of the appellate process is the ability to submit additional supporting documents, such as:

This is critical in NRI cases where non-taxability or treaty relief needs to be substantiated properly.

If an appeal is not filed, the following options may be considered:

Revision under Section 264

Writ Petition before High Court

Applicable in cases involving:

Common in NRI cases where notices are sent to outdated Indian addresses.

Tax Demand Raised? Seek Stay under Section 220(6)

If the assessment results in a tax demand, you should immediately file a:

Stay of Demand Application under Section 220(6)

This helps:

NRIs frequently face adverse assessments due to:

Handling such cases requires specialised expertise in NRI taxation, FEMA, and cross-border tax laws.

Dinesh Aarjav & Associates is a leading Chartered Accountant firm based in Delhi with over 25 years of experience, specialising in NRI services, including:

Receiving an adverse assessment order despite filing a reply is not uncommon. However, the Income Tax Act provides clear appellate and revisionary remedies to challenge such orders.

Timely action, proper documentation, and expert representation can significantly improve the outcome.

If you have received an assessment order under Section 148 or Section 143(3) and believe the additions are incorrect, it is critical to evaluate your appeal options and initiate corrective action immediately.

ITAT Mumbai’s Landmark Ruling: Section 69 Cannot Override Section 5(2)

CA Nitin Jain is an Associate at Dinesh Aarjav & Associates with more than 10 years of experience specializing in NRI taxation, cross-border tax matters, assessments, appeals, and tax litigation. He regularly assists NRIs and international clients in navigating Indian tax compliance requirements and representing them before various tax authorities.

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)