WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

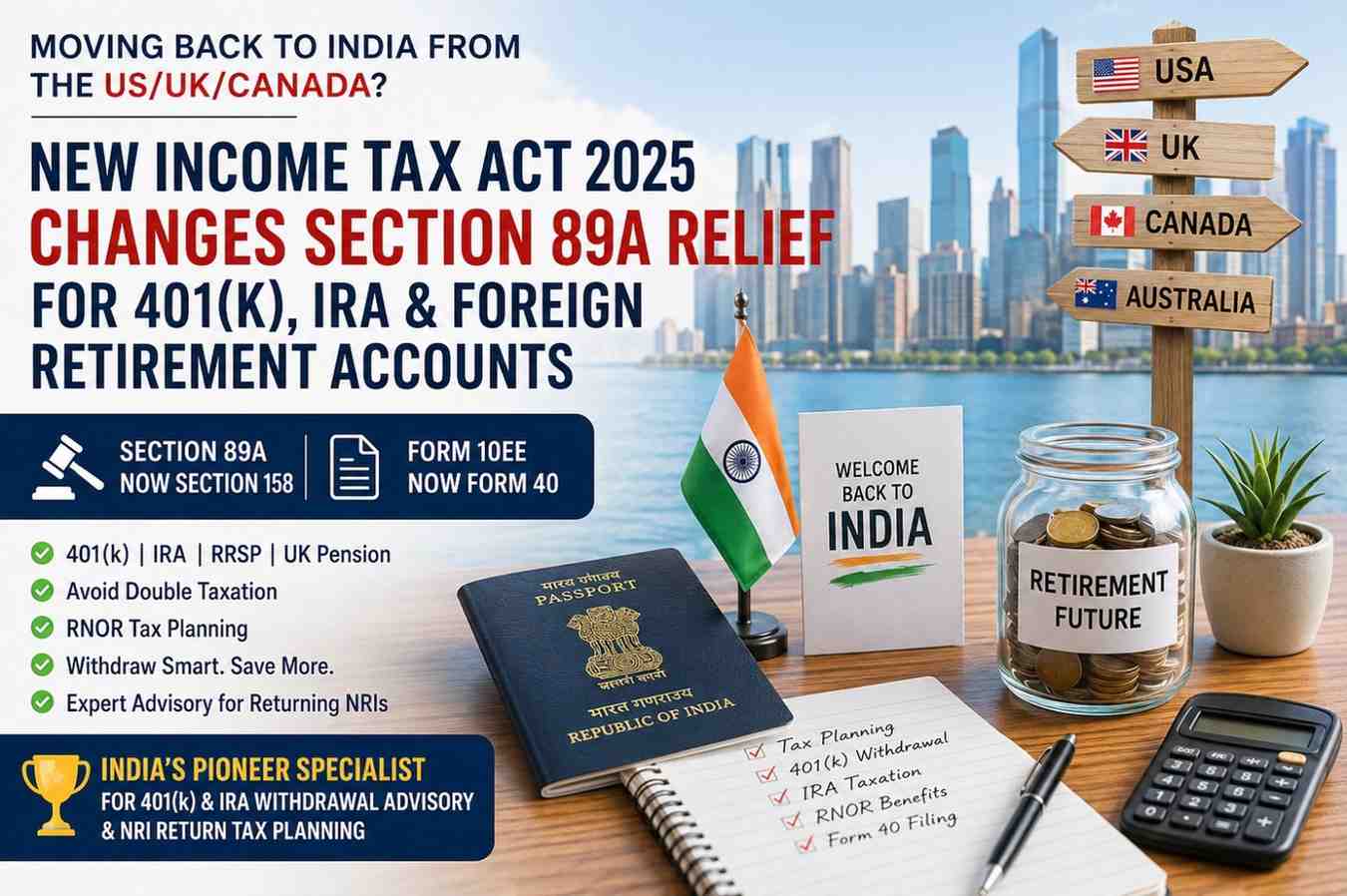

Planning to return to India from the US, UK, or Canada while holding a 401(k), IRA, RRSP, or foreign retirement account? The Income Tax Act, 2025 has introduced an important structural change to how tax relief for foreign retirement accounts will operate in India.

If you are a returning NRI, especially from the United States, United Kingdom, Canada, or Australia, understanding these changes can potentially save you from double taxation, incorrect reporting, tax notices, and costly mistakes while withdrawing retirement savings.

Many NRIs returning to India hold substantial balances in:

The biggest concern?

“Will India tax my retirement account even if I have not withdrawn money?”

This is precisely where Section 89A (old law) and now Section 158 under the Income Tax Act, 2025 become critical.

Under the Income Tax Act, 1961, taxpayers relied on Section 89A to claim relief from taxation on income accrued in specified foreign retirement accounts.

However, under the new Income Tax Act, 2025, Section 89A has now been replaced by Section 158 read with Rule 74 of the Income Tax Rules, 2026.

While the objective remains largely the same, the procedural framework has changed.

The new law continues to provide tax relief on income from foreign retirement benefit accounts maintained in notified countries, helping avoid timing mismatches and double taxation between India and the foreign country.

Before Section 89A came into effect, returning NRIs often faced a major tax issue.

Countries like the US, UK, and Canada typically tax retirement accounts such as 401(k), Traditional IRA, RRSP, and pension plans at the time of withdrawal, whereas India could potentially tax annual accretions, growth, dividends, or accrued income.

This created a double taxation mismatch:

Example:

Result?

Potential double taxation on the same retirement corpus.

To address this, the Government introduced Section 89A, allowing eligible taxpayers to defer Indian taxation until withdrawal, matching the foreign country’s taxation timeline.

The same relief continues under Section 158 of the Income Tax Act, 2025.

Currently, the following countries are notified for relief:

This means if you maintained a retirement account in these countries while being a tax resident there and a non-resident in India, you may be eligible for relief.

Some of the most common foreign retirement accounts eligible for relief include:

For Returning NRIs from USA

For Returning NRIs from Canada

For Returning NRIs from UK

For Returning NRIs from Australia

The research note specifically identifies 401(k) plans and Traditional IRA accounts under the US category.

One of the biggest procedural changes is the replacement of Form 10EE.

Under the old law:

Form 10EE was filed to exercise the option under Section 89A.

Under the new law:

Form 40 must now be filed to exercise the option under Section 158 of the Income Tax Act, 2025.

This change is highly important for returning NRIs with 401(k), IRA, RRSP or UK pension accounts, since failure to file the prescribed form may impact the ability to claim relief.

To claim relief, a taxpayer should generally satisfy the following conditions:

You must be:

A crucial point often missed by returning NRIs:

Once the option is exercised for a tax year, it cannot be withdrawn for that year or subsequent years.

This makes retirement withdrawal planning extremely important.

For example:

A wrong election timing may impact:

This is why strategic advisory becomes critical before filing.

Returning NRIs may need substantial documentation, including:

1. Foreign Retirement Account Details

2. Retirement Account Statements

Supporting evidence showing account details and balances.

3. Foreign Taxability Proof

Documents explaining how the retirement income is taxed or taxable abroad.

4. Prior Tax Computation

Income computations for years where foreign retirement income was already taxed in India.

5. Reconciliation Statements

Reconciliation with prior Indian income tax returns.

Merely filing Form 40 may not be sufficient.

Depending on your facts, disclosures may also arise under:

Schedule FA (Foreign Assets)

Disclosure of:

Schedule FSI (Foreign Source Income)

Reporting foreign income earned.

Schedule Salary / Other Sources

Depending upon whether pension or investment income is involved.

Incorrect disclosure can lead to:

One of the biggest mistakes we see:

Withdrawing retirement funds without planning RNOR vs ROR status

This can significantly alter taxation.

Questions returning NRIs should evaluate:

These questions require case-specific tax modelling.

There is no one-size-fits-all answer.

If you are returning to India from the US, UK, Canada, or Australia, consider the following action points:

Step 1: Review Your Retirement Accounts

Identify:

Step 2: Evaluate RNOR Status

Your RNOR window may create planning opportunities.

Step 3: Assess Withdrawal Timing

Timing could materially impact taxes.

Step 4: File Form 40 Properly

Avoid procedural mistakes.

Step 5: Ensure Correct ITR Reporting

Schedule FA and foreign income reporting should align.

At Dinesh Aarjav & Associates, we advise NRI returning to india from the US, UK, Canada and Australia on:

With 25+ years of experience advising global NRIs, our team helps clients navigate the complex intersection of Indian tax law, DTAA, FEMA, and foreign retirement account taxation.

Is a 529 Plan Worth It for NRIs Moving Back to India? Here's the Reality.

Pre-Immigration Tax Planning Before Moving to USA – Key Financial Checklist for NRIs

Tax Clearance Certificates for Indians Moving Abroad: What You Need to Know

RSU Taxation in the UK for NRIs: Complete Guide to Filing, Double Taxation Relief & Deadlines

CA Priyal Goel Jain is a Partner at Dinesh Aarjav & Associates and a leading expert in India–US cross-border taxation, NRI taxation, and international tax advisory. She advises NRIs, OCIs, and global families on complex cross-border transactions, tax planning, foreign asset reporting, and multi-jurisdictional compliance matters.

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)