WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

If you are an NRI, H1B visa holder, Green Card holder, or US tax resident, and you hold a Public Provident Fund (PPF) account in India, this is something you cannot afford to ignore.

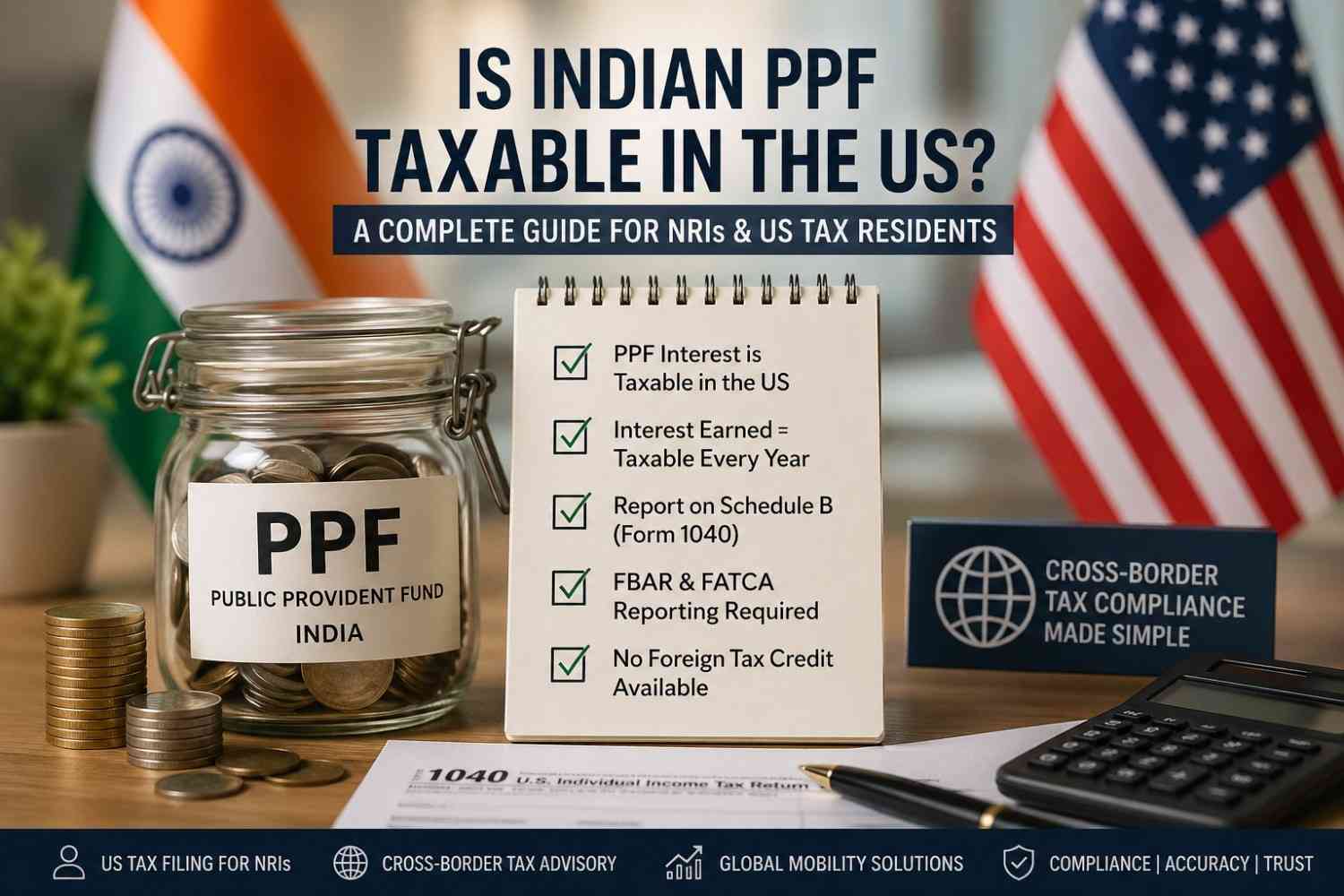

Yes — Indian PPF is taxable in the US.

Even though PPF enjoys EEE (Exempt-Exempt-Exempt) tax status in India, the IRS taxes it annually as foreign income.

The United States taxes worldwide income, regardless of:

The IRS does NOT treat PPF as a qualified retirement account.

Instead, it is viewed as:

Result: PPF interest is taxed as ordinary income in the US

1. Annual Interest is Taxable

Interest is taxed every year, even if:

This follows the accrual method of taxation used by the IRS.

2. Principal Contribution is NOT Taxed

3. Reporting in US Tax Return

You must report PPF income under:

Convert to USD (IRS exchange rate)

Report as taxable interest income in your US return

Under Indian tax law:

Under US tax law:

Since no tax is paid in India, you:

Holding a PPF account may trigger multiple reporting obligations:

1. FBAR (FinCEN Form 114)

Required if total foreign accounts exceed $10,000

2. FATCA (Form 8938)

Required if foreign assets exceed thresholds (higher than FBAR)

3. Schedule B Disclosure

Must disclose foreign accounts and interest income

Non-compliance risks:

These errors often lead to:

If you are:

Then PPF creates:

It must be reviewed as part of your global mobility tax planning

Result: Full US taxation remains

Key considerations:

At Dinesh Aarjav & Associates, we specialize in:

US Tax Filing Services (India-based)

Cross-Border Tax Advisory

Global Mobility & NRI Advisory

With 25+ years of experience, presence across India, US, UK, UAE, Canada & Australia, and 2600+ clients globally, we offer end-to-end cross-border NRI taxation solutions.

While PPF is tax-free in India, it is:

Understanding this difference is critical for NRIs, expats, and global professionals managing finances across India and the US.

If you:

We can assist you with accurate, compliant, and optimized US tax filing from India.

NRI Financial Guide: Essential Questions on PPF and Savings Accounts

PPF Investments for NRIs - A Guide to Tax-Saving Opportunities

If you are an NRI and want to invest in PPF in India? Then this is for you!!

CA Sanyam Goel, CPA (USA), FCA, and CISA, specializes in India–US cross-border taxation, NRI tax advisory, US tax compliance, transfer pricing, and international regulatory matters. He assists clients with US and Indian tax obligations, cross-border reporting requirements, and strategic tax planning for global investments and transactions.

.webp)