WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

One of the most critical yet frequently ignored compliance requirements for Non-Resident Indians (NRIs) is the mandatory conversion of resident savings bank accounts after a change in residential status.

Many individuals who move abroad for employment, business, or higher education continue operating their resident savings accounts in India, assuming there is no immediate risk. However, under the Foreign Exchange Management Act (FEMA), 1999, this is a direct violation of Indian law.

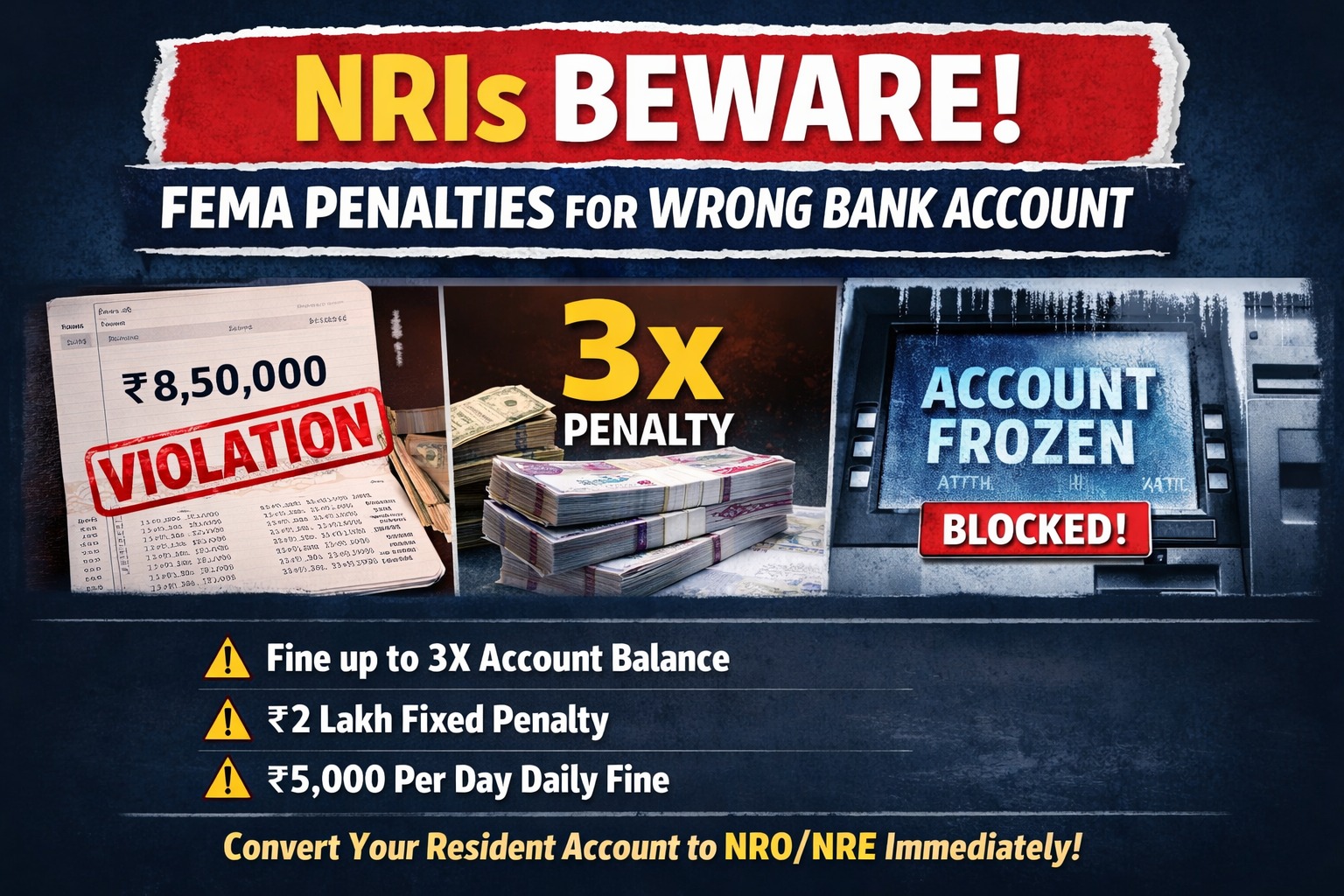

Failure to comply can result in penalties up to 3 times the account balance, fixed fines, daily penalties, and even account freezing by banks.

This article provides a comprehensive explanation of FEMA rules for NRI bank accounts, penalties for non-compliance, and the correct process for converting resident accounts to NRO/NRE accounts.

Under FEMA, residential status is determined based on purpose of stay and intention, not just physical presence.

1. 182-Day Rule Under FEMA

You are considered a non-resident if:

This applies to:

2. Intention to Stay Outside India

Even if the 182-day condition is not met, you qualify as an NRI if you:

Key Insight: Under FEMA, intention overrides duration, making early compliance essential.

As soon as your status changes to NRI:

You may also open:

Continuing to operate a resident account as an NRI is prohibited under FEMA regulations.

Non-compliance with FEMA provisions can trigger severe penalties under Section 13 of FEMA Act, 1999.

1. Penalty Up to 3 Times the Amount Involved

The penalty can be as high as three times the balance in the resident account

2. Fixed Penalty

Where the amount cannot be quantified, a penalty of up to ₹2,00,000 may be imposed

3. Continuing Penalty

An additional ₹5,000 per day is levied for every day the violation continues

Important: These penalties are cumulative and can significantly increase financial exposure over time.

Banks in India conduct periodic KYC and compliance checks. If your residential status is identified as non-resident:

This can impact:

Fixed Deposits and Recurring Deposits

Joint Accounts

Delaying Conversion Until Tax Filing

FEMA compliance is independent of income tax filing. The requirement arises immediately upon change in residential status.

Assuming Small Balances Are Safe

Even with low balances:

Relying on Banks for Notification

Banks are not responsible for informing customers about FEMA status changes.

The compliance responsibility lies entirely with the account holder.

Misunderstanding the 182-Day Rule

Many assume NRI status begins only after 182 days.

However, taking up employment or moving abroad with intent triggers NRI status immediately.

If you have moved abroad, ensure the following actions are completed:

Non-compliance can lead to:

Dinesh Aarjav & Associates provides specialized nri advisory services, including:

With over 25 years of experience in NRI taxation and FEMA regulations, we assist clients globally in maintaining full compliance with Indian laws.

Maintaining a resident savings account after becoming an NRI is not a minor oversight—it is a serious FEMA violation with substantial financial consequences.

Timely action can help avoid:

NRIs should proactively review their banking arrangements and ensure full compliance with FEMA regulations to safeguard their financial interests.

Can NRIs Give or Receive Loans in India? A Complete Guide under FEMA & Income Tax Rules

Trading in US Futures & Options After Returning to India: FEMA, Tax & Compliance Explained

Gifting US Stocks to Parents in India: What You Must Know About Taxes, FEMA, and Compliance

Unlocking Foreign Investment Opportunities: RBI Eases FEMA Regulations for Derivatives

CA Disha Bansal is a tax professional at Dinesh Aarjav & Associates specializing in US taxation, India–US cross-border tax advisory, and NRI tax compliance. She advises individuals and NRIs on US tax return preparation, international reporting requirements, cross-border tax planning, and navigating complex India–US tax matters, helping clients manage their global tax obligations efficiently and compliantly.

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)