WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

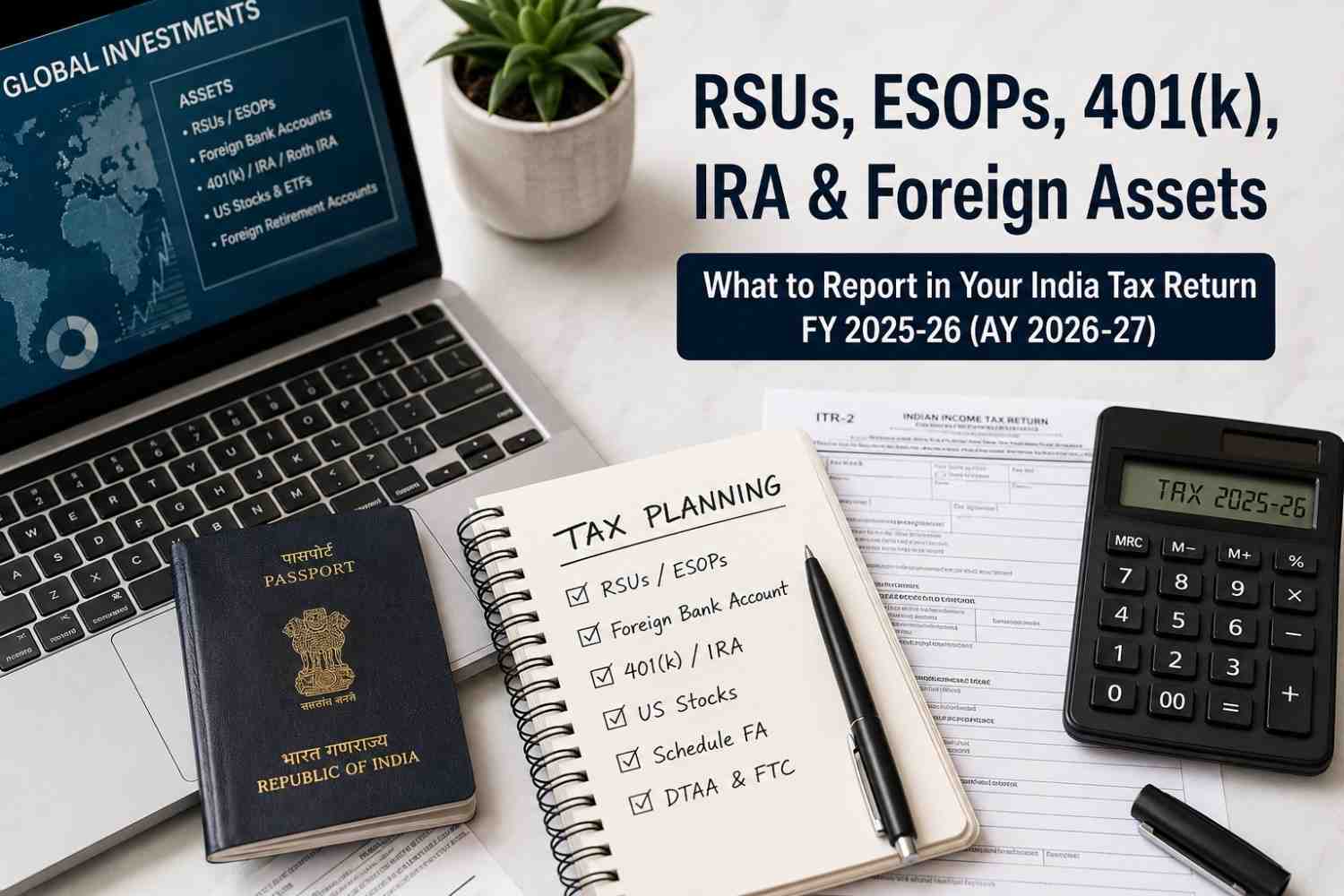

Have RSUs, ESOPs, US stocks, a foreign bank account, IRA, Roth IRA, 401(k), or overseas investments? Filing your India Income Tax Return (ITR) for FY 2025–26 (AY 2026–27) may be more complicated than many taxpayers expect.

With increasing global information sharing through FATCA, CRS (Common Reporting Standard), and tax treaties, the Indian Income Tax Department has significantly greater visibility into overseas financial assets. As a result, foreign asset disclosure, Schedule FA reporting, foreign income reporting, and claiming foreign tax credit have become increasingly important—especially for returning NRIs, H-1B professionals, startup employees, and global executives.

Many taxpayers wrongly assume:

“My income was already taxed abroad, so I don’t need to disclose it in India.”

In reality, incorrect reporting of RSUs, foreign bank accounts, retirement accounts like 401(k) or IRA, and overseas investments may trigger notices, double taxation issues, or compliance gaps.

In this guide, we explain what you may need to report in your India tax return for FY 2025–26, and the key mistakes to avoid.

Your reporting requirement largely depends on your residential status in India.

If You Are Resident and Ordinarily Resident (ROR)

Your global income is generally taxable in India, and foreign asset disclosure obligations become much wider.

This may include:

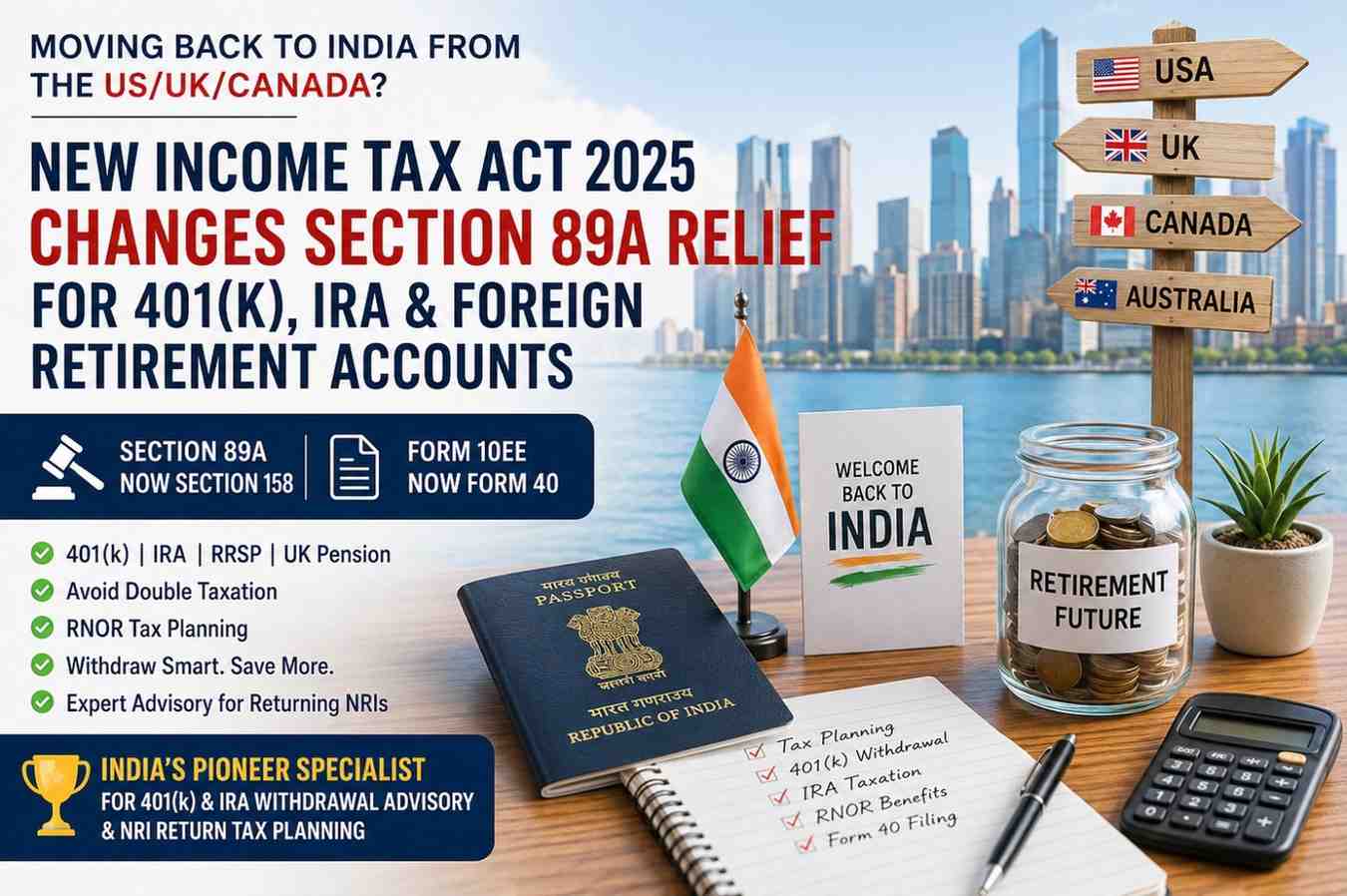

For many returning NRIs, RNOR status can provide tax relief on certain foreign income.

However:

RNOR does not automatically mean “nothing needs to be reported.”

Taxability and disclosure obligations should be evaluated carefully based on the asset, source of income, and treaty position.

Employees of multinational companies often hold:

If you worked in the US, UK, Canada, UAE, Singapore, or Europe, your equity compensation may require tax review in India.

RSU taxation in India depends on factors such as:

In many cases:

Even if taxes were deducted abroad, you may still need to:

One of the most common mistakes made by returning professionals is forgetting to report RSUs or ESOPs in their India tax return.

Do you still maintain:

These may require review for foreign asset disclosure in ITR, especially for resident taxpayers.

Depending on your residential status, foreign accounts may require disclosure under Schedule FA of ITR.

Even dormant or low-balance accounts are often overlooked.

If you hold:

income such as:

may need tax evaluation in India.

One of the biggest concerns for returning Indians is:

“Do I need to disclose my 401(k) or IRA in India?”

Is 401(k) Taxable in India?

The answer depends on:

Is IRA Taxable in India?

For Traditional IRA and Roth IRA, taxation depends on:

Many returning Indians mistakenly assume:

“Retirement money becomes taxable only when I transfer it to India.”

In reality, taxability and reporting requirements may require careful planning—especially while transitioning from RNOR to ROR status.

Schedule FA (Foreign Assets) is the section in the Income Tax Return where qualifying taxpayers disclose overseas financial interests.

This may include:

Incorrect reporting of Schedule FA is one of the biggest compliance mistakes in cross-border tax filing.

If taxes have already been paid abroad on:

you may be eligible for relief through:

DTAA (Double Taxation Avoidance Agreement)

or

Foreign Tax Credit (FTC)

India has tax treaties with countries including the USA, UK, Canada, UAE, Singapore, and Australia.

In many cases, Form 67 also becomes relevant for claiming foreign tax credit.

These mistakes may lead to notices, scrutiny, or avoidable double taxation.

If you have:

it is advisable to review both taxability and disclosure requirements before filing your return.

At Dinesh Aarjav & Associates, we assist NRIs, NRI returning to india, H-1B professionals, OCI card holders, and globally mobile families with:

Q.1 Do I need to report RSUs in India tax return?

Ans: If you are a tax resident in India, reporting and taxation may apply depending on vesting and sale.

Q.2 Do I need to disclose a foreign bank account in ITR?

Ans: In many cases, yes—particularly for resident taxpayers.

Q.3 Is 401(k) taxable in India?

Ans: Taxability depends on residential status, timing of withdrawal, and treaty provisions.

Q.4 Is Roth IRA taxable in India?

Ans: Indian tax treatment depends on facts, tax residency, and withdrawal structure.

Q.5 What is Schedule FA?

Ans: Schedule FA is the foreign asset disclosure section in Indian Income Tax Return.

Q.6 Can I claim tax credit for taxes paid abroad?

Ans: Yes, subject to DTAA provisions and Foreign Tax Credit rules.

If you hold RSUs, ESOPs, IRA, 401(k), foreign retirement accounts, overseas investments, or foreign bank accounts, our cross-border tax team can help ensure compliant and tax-efficient reporting.

RSU Taxation in the UK for NRIs: Complete Guide to Filing, Double Taxation Relief & Deadlines

Everything You Need to Know About Taxation of Restricted Stock Units (RSUs) Taxation in India

URGENT: Income Tax Notice for Foreign Assets, 401(k), RSUs or Overseas Accounts?

Understanding FBAR Filing: A Crucial Tax Obligation for NRIs in the US

.webp)