WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

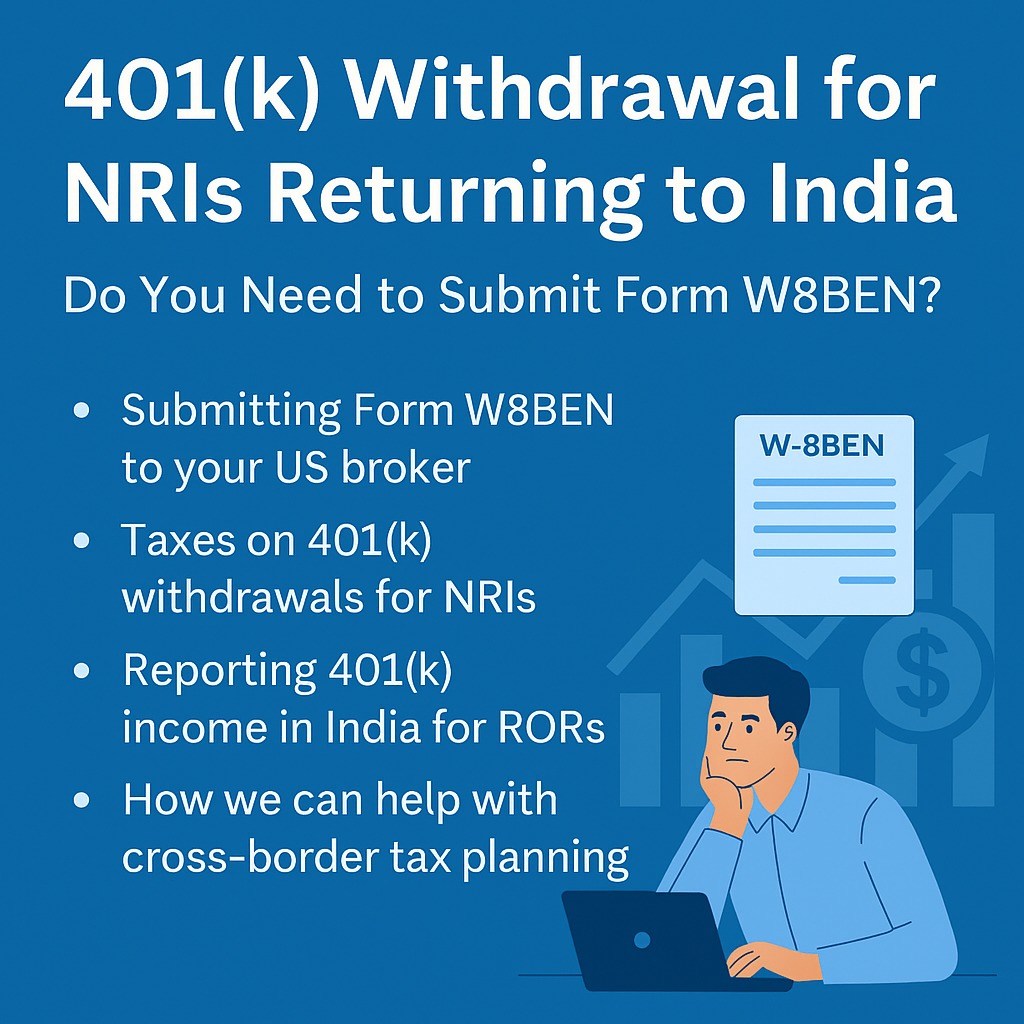

Are you an NRI (Non-Resident Indian) who has moved back to India and is now planning to withdraw funds from your 401(k) retirement account in the United States? Or are you still abroad but planning a 401(k) distribution soon?

Understanding the tax implications, disclosure requirements, and compliance obligations in both the US and India is crucial—especially if you now hold Resident and Ordinarily Resident (ROR) status in India.

In this guide, we explain the role of Form W8BEN, applicable withholding tax, reporting obligations in India, and most importantly—how Dinesh Aarjav & Associates can help you in making your 401(k) withdrawal smooth, compliant, and tax-efficient.

Yes, Form W8BEN is essential before making a 401(k) withdrawal if you are a non-resident of the United States. This IRS form certifies that:

Although submitting W8BEN is mandatory, please note that the India-US DTAA does not offer a reduced withholding tax rate specifically for 401(k) accounts. As a result, most plan administrators or brokers will withold a flat 30% tax on the gross amount withdrawn.

After W8BEN submission, and once the 401(k) distribution is processed, here's what you can expect:

If you have made a 401(k) withdrawal, you must file Form 1040-NR (U.S. Nonresident Alien Income Tax Return) to report the income and calculate your final tax liability. The Contributions and earnings taxed at graduated slab rates

This filing is crucial to avoid double taxation, and to potentially claim any refund if excess tax was withheld.

If you’ve returned to India and have become a Resident and Ordinarily Resident (ROR) under Indian tax law, your global income becomes taxable in India. This includes foreign retirement accounts like 401(k).

File Form 67 online on the Income Tax Portal before filing your ITR

At Dinesh Aarjav & Associates, we specialize in cross-border tax planning for NRIs, OCIs, and returning Indian residents. Our expert team offers end-to-end support for 401(k) withdrawals, ensuring you stay fully compliant in both India and the US.

Whether you are withdrawing a lump sum or planning systematic withdrawals from your 401(k) after returning to India, we ensure complete peace of mind with expert tax advisory.

| Step | Action |

| Step 1 | Submit Form W8BEN to US broker |

| Step 2 | Initiate 401(k) withdrawal – expect 30% withholding |

| Step 3 | File Form 1040-NR in the US for the year of withdrawal |

| Step 4 | Determine your residential status (ROR/NRI) in India |

| Step 5 | Report 401(k) income in Schedule FA, FSI, OS/CG, TR |

| Step 6 | File Form 67 to claim foreign tax credit in India |

| Step 7 | Consider tax optimization and structuring with expert help |

Handling a 401(k) withdrawal while transitioning from an NRI to an Indian tax resident requires careful planning, documentation, and tax compliance. Filing Form W8BEN, paying US taxes, and disclosing the 401(k) correctly in your Indian ITR are all essential steps.

At Dinesh Aarjav & Associates, we help you navigate this process seamlessly—ensuring that you stay fully compliant with IRS, Indian Income Tax Department, and DTAA provisions.

Let us help you withdraw your 401(k) with confidence.

CA Priyal Goel Jain is a Partner at Dinesh Aarjav & Associates and a leading expert in India–US cross-border taxation, NRI taxation, and international tax advisory. She advises NRIs, OCIs, and global families on complex cross-border transactions, tax planning, foreign asset reporting, and multi-jurisdictional compliance matters.

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)