WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

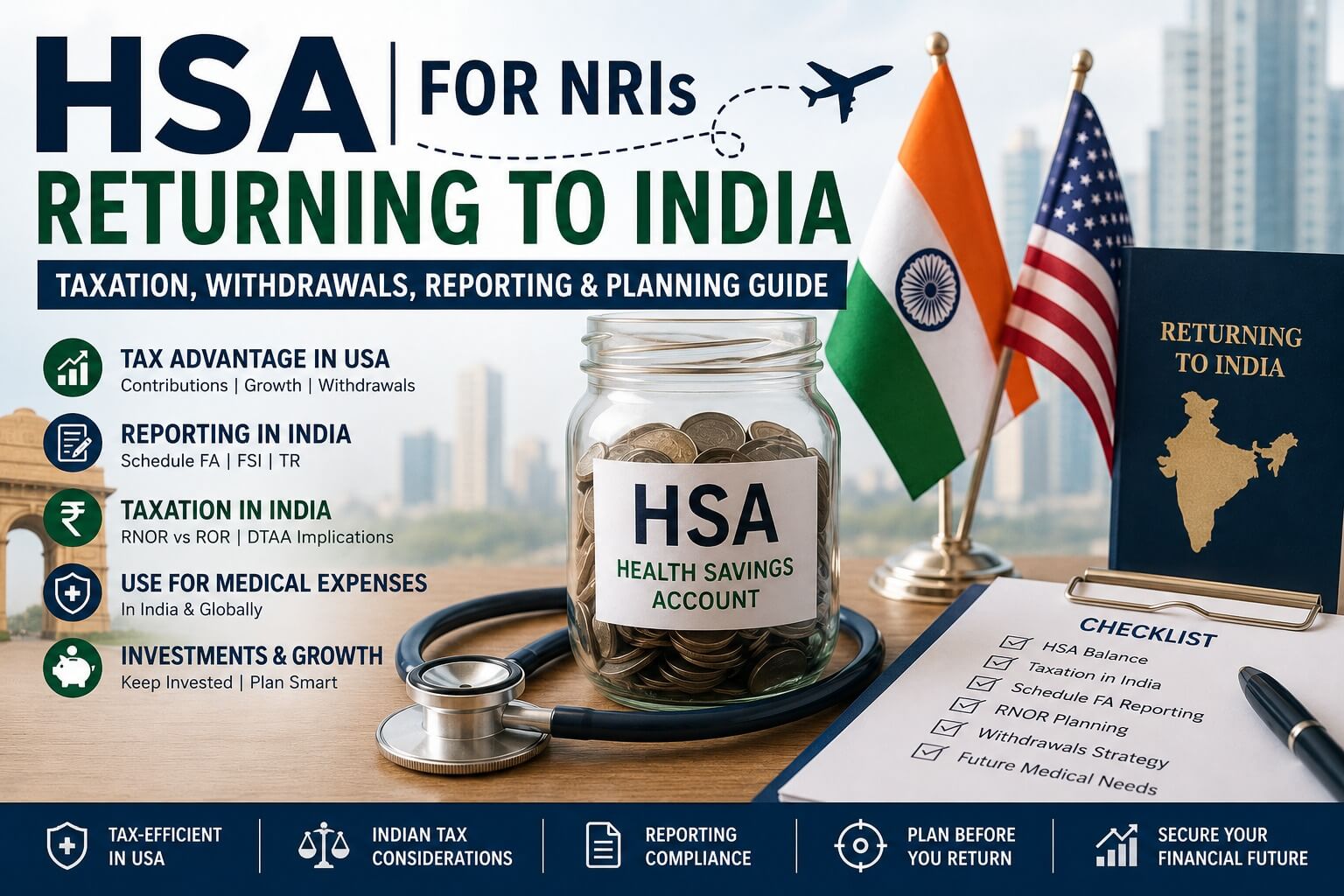

If you are an NRI, H-1B professional, Green Card holder, U.S. citizen, OCI holder, or Indian American planning to return to India, your Health Savings Account (HSA) deserves careful attention.

Many returning Indians focus on:

An HSA can remain one of the most valuable assets accumulated during your years in the United States. However, India does not specifically recognize HSA tax benefits in the same manner as the U.S. Internal Revenue Code.

This creates important questions regarding:

This guide covers everything NRIs need to know before, during, and after relocating to India.

A Health Savings Account (HSA) is a tax-advantaged savings account available to individuals enrolled in a High Deductible Health Plan (HDHP) in the United States.

An HSA is often considered one of the most powerful tax-efficient investment vehicles available under U.S. tax law because it offers a rare triple tax advantage.

Tax-Deductible Contributions

Contributions generally reduce taxable income in the United States.

Tax-Deferred Growth

Interest, dividends, and investment gains accumulate without current U.S. taxation.

Withdrawals used for eligible medical expenses are generally tax-free in the United States.

Because of these advantages, many professionals working in the U.S. accumulate substantial HSA balances before returning to India.

Many returning NRIs spend months planning:

Without proper planning, an HSA may create uncertainty regarding:

A well-structured return-to-India strategy should always include HSA planning.

Yes.

In most situations, your HSA does not automatically close simply because you relocate outside the United States.

Many HSA custodians allow account holders to continue maintaining their accounts after moving abroad.

You can generally:

The key question is not whether the account can remain open.

The more important question is how the account will be treated under Indian tax laws after your return.

Generally, new HSA contributions require:

Most individuals who permanently relocate to India cease participation in a U.S. qualifying health plan and therefore typically lose eligibility for future HSA contributions.

However, existing balances generally remain invested.

Many HSA accounts contain substantial investments accumulated over years.

Common HSA investments include:

These investments can often continue growing even after relocation.

The challenge arises because the tax treatment of this growth under Indian law may differ significantly from U.S. treatment.

This is one of the most important questions for returning NRIs.

India currently does not provide specific recognition to Health Savings Accounts under the Income-tax Act.

As a result, several questions arise:

The answers depend on:

This is why HSA planning should be integrated with broader India-US tax planning.

One of the most valuable tax planning opportunities for returning NRIs is Resident but Not Ordinarily Resident (RNOR) status.

During RNOR years, certain foreign income may continue receiving favorable treatment under Indian tax rules.

This creates planning opportunities regarding:

For many NRIs, the RNOR window becomes the ideal period to review HSA strategy before transitioning to full Indian tax residency.

Once RNOR benefits end, taxpayers generally become Resident and Ordinarily Resident (ROR).

At this stage:

This transition often represents the most critical stage for long-term HSA planning.

Potentially yes.

Many returning Indians focus on reporting:

but fail to evaluate HSA reporting obligations.

Depending upon your facts and circumstances, an HSA may need consideration under:

Foreign account disclosure requirements may apply.

Schedule FSI (Foreign Source Income)

Foreign income reporting may become relevant.

Schedule TR (Tax Relief)

Foreign tax credit considerations may arise in certain situations.

Proper disclosure is critical to avoid future compliance issues.

Schedule FA is one of the most important disclosure schedules for Indian residents holding overseas assets.

Returning Indians often ask:

The answers depend on the structure of the account and the taxpayer's residential status.

Failure to properly review foreign asset reporting requirements can create unnecessary compliance risks.

Yes.

Many NRIs eventually utilize HSA funds for:

However, maintaining proper records remains essential.

Documentation often becomes important when substantiating the tax treatment of withdrawals.

One of the most searched questions by returning NRIs is:

Can I withdraw my HSA after moving to India?

Generally yes.

However, tax treatment may depend on:

Every withdrawal strategy should be reviewed in the context of overall retirement planning.

Not necessarily.

In reality, withdrawing funds before relocation may not always be the most tax-efficient strategy.

Factors to evaluate include:

A customized analysis generally produces better outcomes than a one-size-fits-all approach.

Both accounts deserve careful planning.

| Factor | HSA | 401(k) |

| Healthcare Focus | Yes | No |

| Tax-Free Medical Withdrawals | Yes | No |

| Investment Growth | Yes | Yes |

| Indian Tax Recognition | Limited | More Established |

| Reporting Complexity | Higher | Moderate |

| RNOR Planning Opportunities | Significant | Significant |

For many returning Indians, HSA planning is often more nuanced than 401(k) planning.

Many NRIs compare these two tax-efficient accounts.

HSA

Designed primarily for healthcare funding.

Roth IRA

Designed primarily for retirement planning.

Both can remain important after relocating to India, but each requires separate tax analysis.

The best planning opportunities often exist before relocation.

Mistake 2: Assuming India Recognizes HSA Benefits

Indian tax treatment may differ significantly from U.S. treatment.

Mistake 3: Missing Schedule FA Disclosure

Foreign asset reporting should always be reviewed carefully.

Mistake 4: Liquidating Investments Without Analysis

Selling investments prematurely may not be optimal.

Mistake 5: Ignoring RNOR Planning

RNOR status can significantly impact outcomes.

Mistake 6: Forgetting About Future Medical Costs

Healthcare expenses often rise during retirement.

Mistake 7: Not Coordinating HSA, IRA and 401(k) Planning

Cross-border retirement planning should be holistic.

A software engineer accumulated a $60,000 HSA balance over ten years and planned to relocate permanently to India.

Proper RNOR planning helped evaluate reporting obligations and future withdrawal strategies.

After retirement, a Green Card holder planned to use HSA assets for healthcare expenses in India.

Returning Indian Family Moving from California

The family had:

Coordinating all accounts before relocation created a more tax-efficient return-to-India strategy.

Our India-US tax specialists assist with:

A Health Savings Account can be one of the most valuable assets accumulated during a professional's time in the United States.

However, once an NRI returns to India, questions surrounding taxation, reporting, withdrawals, foreign asset disclosure, RNOR status, and long-term retirement planning become increasingly important.

The most successful return-to-India transitions involve proactive planning before relocation, careful evaluation during RNOR years, and a coordinated strategy that integrates HSA, IRA, 401(k), brokerage accounts, and overall India-US tax considerations.

For NRIs, Indian Americans, Green Card holders, H-1B professionals, and returning Indians, a properly structured HSA strategy can preserve flexibility, improve tax efficiency, and support long-term healthcare and retirement objectives.

CA Priyal Goel Jain is a Partner at Dinesh Aarjav & Associates and a leading expert in India–US cross-border taxation, NRI taxation, and international tax advisory. She advises NRIs, OCIs, and global families on complex cross-border transactions, tax planning, foreign asset reporting, and multi-jurisdictional compliance matters.

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)