WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

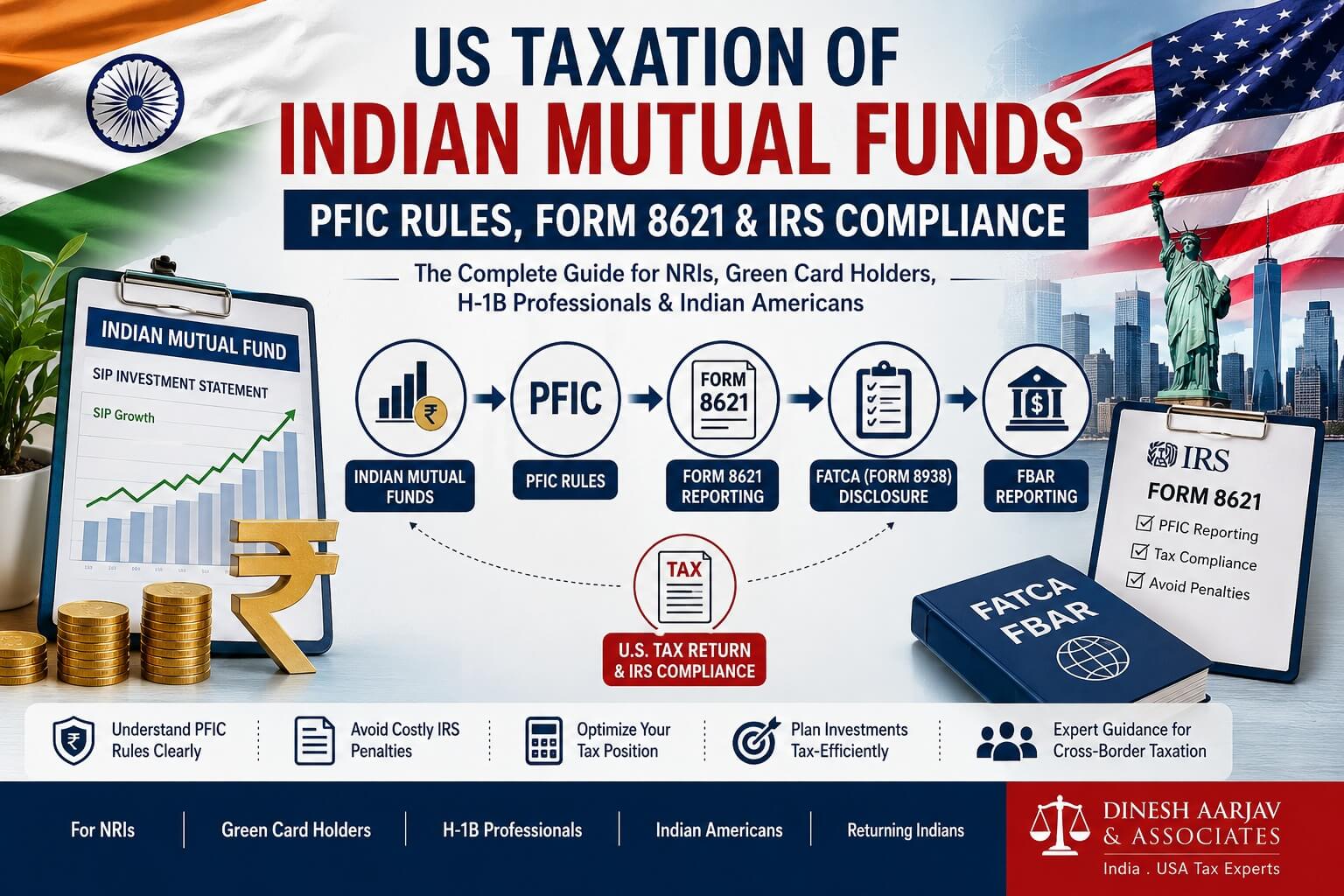

However, what many investors do not realize is that these seemingly simple investments can trigger one of the most complex areas of the U.S. tax code: the Passive Foreign Investment Company (PFIC) regime.

This classification can lead to complex annual reporting, additional tax calculations, IRS Form 8621 filing requirements, and potentially higher taxes compared to similar investments held through U.S.-domiciled funds.

This comprehensive guide explains everything NRIs, Green Card Holders, U.S. citizens, Indian Americans, and returning Indians need to know about PFIC taxation of Indian mutual funds.

A Passive Foreign Investment Company (PFIC) is a non-U.S. corporation that satisfies either of the following IRS tests:

Income Test

At least 75% of the corporation’s gross income is passive income.

Asset Test

At least 50% of the corporation’s assets generate or are held to generate passive income.

Since Indian mutual funds primarily hold investment assets and generate passive investment income, they typically meet one or both PFIC tests.

As a result, most Indian mutual funds are classified as PFICs for U.S. tax purposes.

PFIC rules were introduced by the IRS to discourage U.S. taxpayers from deferring taxes through offshore investment structures.

Unfortunately, these rules often impact ordinary investors who simply continue holding investments in India after moving to the United States.

Many NRIs discover PFIC rules only after several years of SIP investments, at which point they may have multiple years of unfiled Form 8621 reporting requirements.

A portfolio consisting of several Indian mutual funds accumulated over years can create dozens of separate PFIC reporting obligations.

Many investors incorrectly assume PFIC rules apply only to mutual funds.

In reality, several Indian investment products may qualify as PFICs.

This distinction is critical because direct stock ownership generally avoids PFIC treatment while mutual fund ownership often does not.

Example: How PFIC Rules Impact an NRI

Suppose an individual moved to the United States in 2021 while continuing SIP investments in Indian mutual funds.

Over time:

Although the gains may qualify for favorable taxation in India, PFIC rules can significantly alter the U.S. tax treatment.

The investor may also be required to file Form 8621 annually for each PFIC investment.

The IRS provides three primary methods for taxing PFIC investments.

Understanding these methods is critical for tax planning.

1. Excess Distribution Method (Default PFIC Regime)

This is the default PFIC taxation method.

Under this approach:

This is generally considered the most punitive PFIC taxation method.

A QEF election allows taxpayers to report their share of PFIC earnings annually.

Potential benefits include:

However, a major challenge exists.

Most Indian mutual funds do not provide the detailed annual PFIC information statements required to support a QEF election.

As a result, this election is often difficult to implement in practice.

Where eligible, taxpayers may elect mark-to-market treatment.

Under this method:

However, eligibility depends on whether the investment qualifies as marketable stock under IRS regulations.

IRS Form 8621: The Most Important PFIC Compliance Requirement

Form 8621 is one of the most complex international tax forms administered by the IRS.

It is used to report PFIC ownership and related income.

Depending on circumstances, Form 8621 may be required when:

Many taxpayers mistakenly believe that reporting Indian mutual funds on FBAR or FATCA forms is sufficient.

In reality, Form 8621 represents an entirely separate reporting requirement.

Failure to properly address PFIC reporting can create significant compliance issues.

Many NRIs confuse these reporting regimes.

Each serves a different purpose.

|

Requirement |

Form 8621 |

Form 8938 |

FBAR |

|

Reports PFIC Ownership |

Yes |

No |

No |

|

Reports Foreign Assets |

Limited |

Yes |

No |

|

Reports Foreign Financial Accounts |

No |

Sometimes |

Yes |

|

Filed With |

IRS |

IRS |

FinCEN |

|

Purpose |

PFIC Reporting |

Foreign Asset Reporting |

Foreign Account Reporting |

In many situations, a taxpayer may need to file all three.

One of the biggest complications for Indian Americans and NRIs is SIP investing.

Every SIP installment may represent a separate PFIC acquisition.

Over several years, a monthly SIP can create:

This is one reason why PFIC compliance often becomes expensive and time-consuming.

Yes, in most cases.

The tax-saving nature of ELSS funds under Indian tax law does not change their classification under U.S. tax rules.

Even though ELSS funds offer deductions in India, they are generally treated as PFICs for U.S. tax purposes.

Generally yes.

Many investors incorrectly assume ETFs avoid PFIC rules.

If the ETF is organized outside the United States and primarily generates passive investment income, it may still qualify as a PFIC.

Each investment should be evaluated individually.

Potentially.

Many ULIPs combine insurance features with investment components.

Depending on their structure, the underlying investments may trigger PFIC considerations.

This area requires specialized analysis because both PFIC and foreign insurance reporting issues may arise.

They are not.

U.S.-domiciled mutual funds and Indian mutual funds are subject to entirely different tax regimes.

Mistake 2: Ignoring Old SIP Investments

Many individuals continue holding SIPs after relocating to the United States without realizing PFIC implications.

Mistake 3: Not Maintaining Historical Purchase Records

Accurate acquisition records are critical for PFIC calculations.

Mistake 4: Selling Before Obtaining Tax Advice

A sale can trigger significant PFIC consequences.

Planning beforehand is often beneficial.

Mistake 5: Missing Form 8621 Filing Requirements

This is among the most common PFIC compliance issues.

Mistake 6: Ignoring Family-Held Investments

PFIC exposure may arise through jointly held or inherited investments.

Mistake 7: Assuming FBAR Reporting Is Sufficient

FBAR does not replace Form 8621.

Mistake 8: Ignoring ULIPs

Certain ULIPs may create both PFIC and foreign insurance reporting issues.

Mistake 9: Assuming ELSS Funds Are Exempt

Tax benefits in India do not create exemptions under U.S. tax law.

Mistake 10: Seeking Advice Only After Receiving an IRS Notice

PFIC planning is most effective when performed proactively.

Many U.S. taxpayers choose to minimize PFIC exposure through alternative investment structures.

Potential options may include:

Many U.S.-listed ETFs provide international diversification without PFIC complications.

These may offer exposure to Indian markets while avoiding PFIC treatment.

Professionally Structured Cross-Border Portfolios

A coordinated India-U.S. investment strategy can reduce compliance burdens and improve after-tax outcomes.

Many taxpayers discover PFIC obligations years after becoming U.S. tax residents.

The appropriate course of action depends on:

Corrective action may be available, but every case requires individual review.

PFIC reporting is one of the most complex areas of cross-border taxation.

At Dinesh Aarjav & Associates, our India-U.S. tax team assists:

Our services include:

Indian mutual funds can be highly effective investments for Indian residents, but for U.S. taxpayers they often introduce significant PFIC complexity.

Understanding PFIC rules before investing—or before selling existing investments—can help avoid costly surprises, reduce compliance risks, and improve long-term tax efficiency.

If you are an NRI, Green Card Holder, H-1B professional, U.S. citizen, or Indian American holding Indian mutual funds, obtaining professional PFIC guidance can help ensure full compliance with IRS requirements while optimizing your overall India-U.S. tax position.

CA Sanyam Goel, CPA (USA), FCA, and CISA, specializes in India–US cross-border taxation, NRI tax advisory, US tax compliance, transfer pricing, and international regulatory matters. He assists clients with US and Indian tax obligations, cross-border reporting requirements, and strategic tax planning for global investments and transactions.

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)