WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

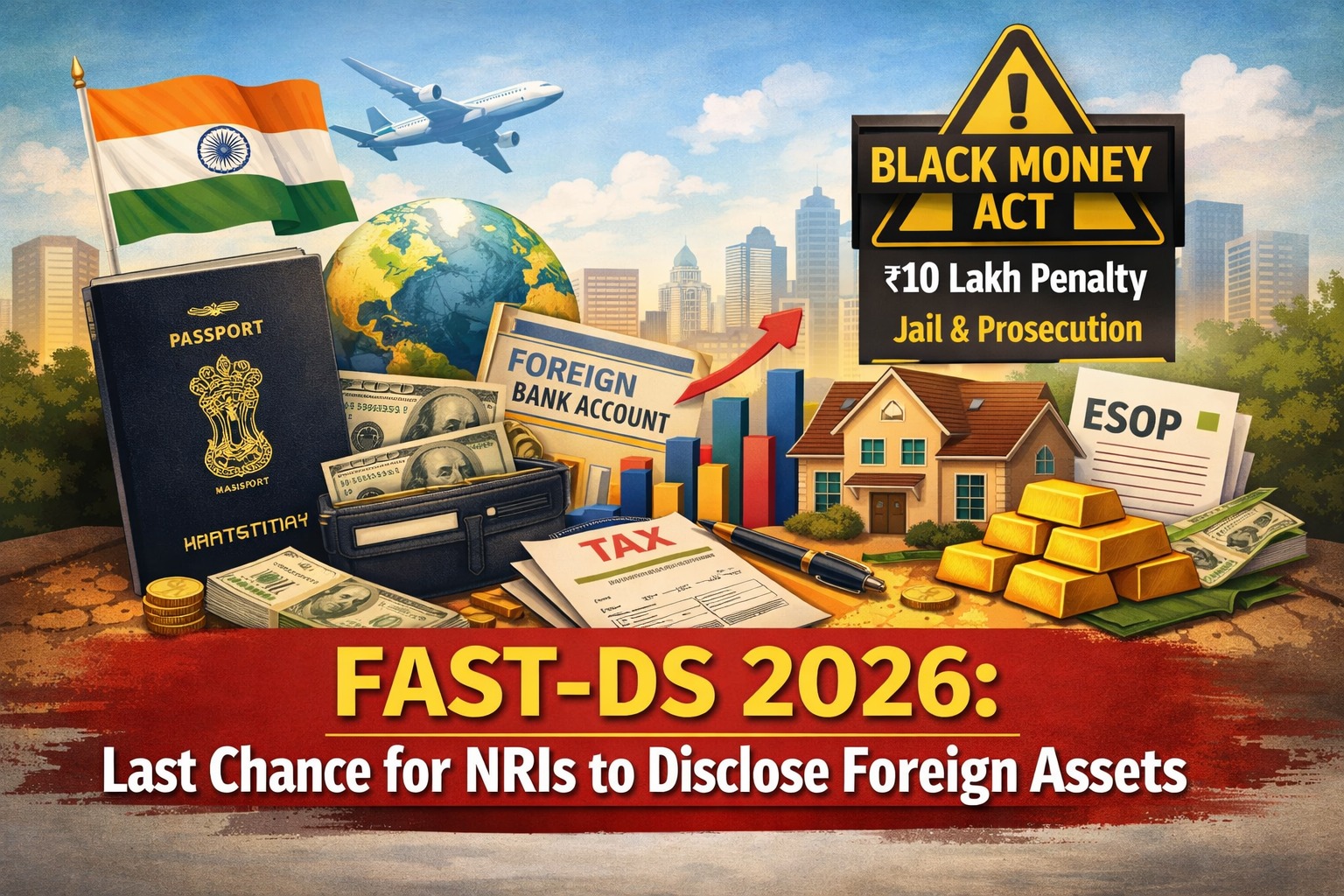

Avoid Black Money Act Penalties | One-Time Amnesty for NRIs & Returning Indians

The Finance Bill, 2026 has introduced one of the most important compliance schemes for NRIs in the last decade — the FAST-DS 2026 (Foreign Assets of Small Taxpayers Disclosure Scheme, 2026).

This one-time disclosure scheme allows NRIs, returning NRIs, RNORs, and resident Indians to disclose undisclosed or incorrectly reported foreign assets and foreign income and obtain complete immunity from penalty and prosecution under the Black Money Act.

If you have ever worked abroad, held a foreign bank account, received ESOPs/RSUs, or owned overseas property, this scheme is extremely critical.

FAST-DS 2026 is a special amnesty-style compliance window introduced under Chapter IV of the Finance Bill, 2026, specifically targeting small taxpayers with foreign asset reporting lapses.

It addresses:

In return for voluntary disclosure, the Government grants:

For NRIs and returning Indians, foreign asset reporting rules make foreign asset compliance the biggest tax risk today.

Under the Black Money (Undisclosed Foreign Income and Assets) Act:

FAST-DS 2026 is effectively a last chance to clean up past mistakes legally.

FAST-DS 2026 operates through two distinct categories, depending on the nature of non-compliance.

This applies where:

Eligibility

Amount Payable

What You Get

Amount paid is non-refundable.

This is the largest and most common NRI mistake.

Applies where:

Eligibility

Amount Payable

What You Get

This is a huge relief for honest NRIs.

Under the scheme, taxpayers must fully and accurately disclose:

Foreign Assets

Foreign Income

Disclosure must be done through:

Applicable returns:

Incorrect schedules = invalid disclosure

Partial disclosure = loss of immunity

The Finance Bill, 2026 also provides relaxation in prosecution for:

This relief is particularly relevant for:

Relief applies only if corrected now.

If you skip this window:

Black Money Act Consequences Resume

The cost of ignoring FAST-DS 2026 is financially and criminally devastating.

Before opting for the scheme, NRIs and Nri returning to india should:

FAST-DS 2026 filings are:

A wrong filing can:

Rule of Thumb for NRIs

If in doubt, disclose.

Compliance under FAST-DS 2026 is far cheaper than prosecution under the Black Money Act.

💡 Pro Tip: If you're planning a complete return to India and need to coordinate taxes with other relocation tasks, use the DesiReturn Planner to create a comprehensive timeline.

At Dinesh Aarjav & Associates, we specialise in:

We handle:

FAST-DS 2026 is not optional for NRIs with foreign assets.

It is a once-in-a-lifetime compliance reset.

If you miss this window, penalties turn brutal and irreversible.

Reach out to us now before the disclosure window closes.

Budget 2026: Major Relief for NRIs Selling Property in India – TDS Compliance Simplified

How Much Gold Can an NRI Bring to India in 2026? Latest Budget 2026 Update on Gold Jewellery

Aarjav Jain is the Executive Director at Dinesh Aarjav & Associates, specializing in India–US cross-border transactions, NRI taxation, international tax advisory, and global investment structuring. With over 10 years of experience in project financing and cross-border advisory, he assists NRIs and businesses with regulatory compliance, repatriation planning, and international transaction structuring.

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)