WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

Are you an Indian investor grappling with high taxes on mutual fund gains? A recent Income Tax Appellate Tribunal (ITAT) ruling might offer a silver lining for Non-Resident Indians (NRIs). But before you pack your bags to shift abroad for tax benefits, understand the nuances that come with this potential tax-saving strategy. Here's a complete guide on how NRIs can legally avoid taxes on mutual fund capital gains in India—without inviting trouble from the tax authorities.

India has Double Taxation Avoidance Agreements (DTAA) with several countries, allowing NRIs to avoid paying tax twice—once in India and again in their country of residence. The key provision that allows for tax exemption is known as the "residual clause" in Article 13 of certain DTAAs.

According to this clause, capital gains (other than those from immovable property and shares) are taxed only in the country of residence of the seller. This means that if you're a tax resident of a country like Singapore, UAE, Mauritius, Portugal, Spain, or the Netherlands, you could potentially enjoy zero tax liability on mutual fund gains in India.

In a recent case, an NRI based in Singapore declared over ₹1.35 crore in capital gains from debt and equity mutual funds and claimed exemption under the DTAA with India. Initially, the Indian tax authorities denied the exemption, arguing that mutual fund units derive value from Indian assets and hence should be taxed in India. However, with proper DTAA consultancy, the taxpayer successfully demonstrated eligibility under the residual clause, which ultimately led to a favorable ruling by the ITAT.

However, the ITAT ruled in favor of the taxpayer, citing that mutual fund units are issued by trusts, not companies, and hence, do not qualify as shares. As a result, these gains fall under the residual clause and are not taxable in India.

This ruling clarified existing laws and sparked interest among resident Indians considering a shift in domicile to save on taxes.

While the ITAT ruling makes tax exemption on mutual funds more accessible for NRIs, experts advise strong caution before relocating solely for tax savings.

Shifting abroad only to save taxes on mutual fund gains may seem tempting, but without a genuine long-term plan, it could backfire. Always consider the legal, logistical, and financial complexities before making such a move.

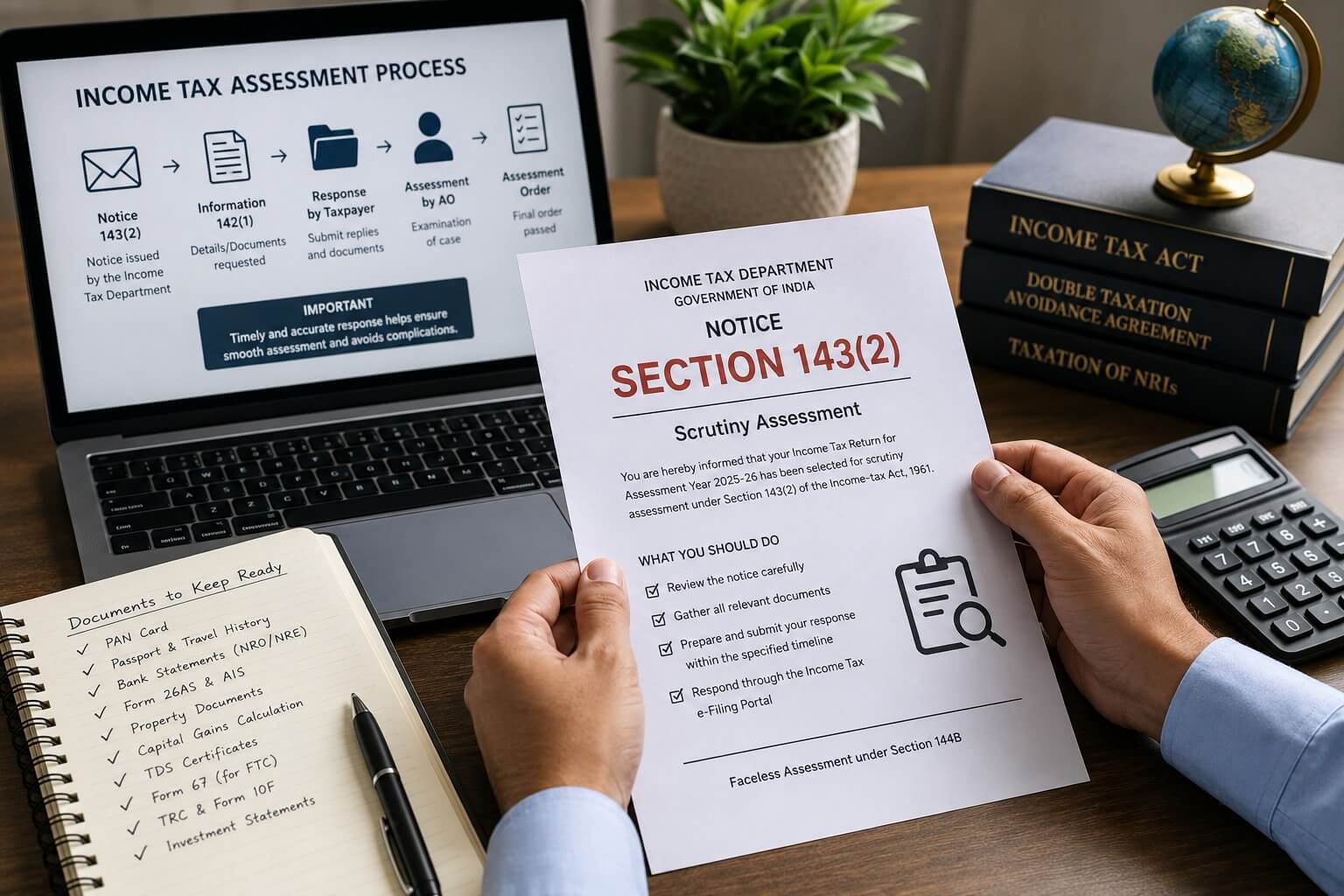

To legitimately claim this tax exemption, NRIs must follow a systematic procedure:

Mutual funds deduct TDS on capital gains for NRIs at applicable rates, regardless of the investor’s income slab. If PAN is not furnished, TDS is deducted at a higher rate. However, you can claim a refund of excess tax by filing your income tax return in India.

Tax planning for NRIs is a legitimate and crucial exercise, but it must be backed by genuine residency and documentation. While mutual funds remain a strong avenue for NRI investment, it's vital to consult a qualified tax advisor to avoid pitfalls and remain compliant.

Dinesh Aarjav & Associates offers end-to-end NRI tax advisory services, including DTAA benefit claims, Form 10F filing, and capital gains advisory.

Looking for expert guidance on NRI taxation and mutual fund investments? Contact us at www.dineshaarjav.com

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)