WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

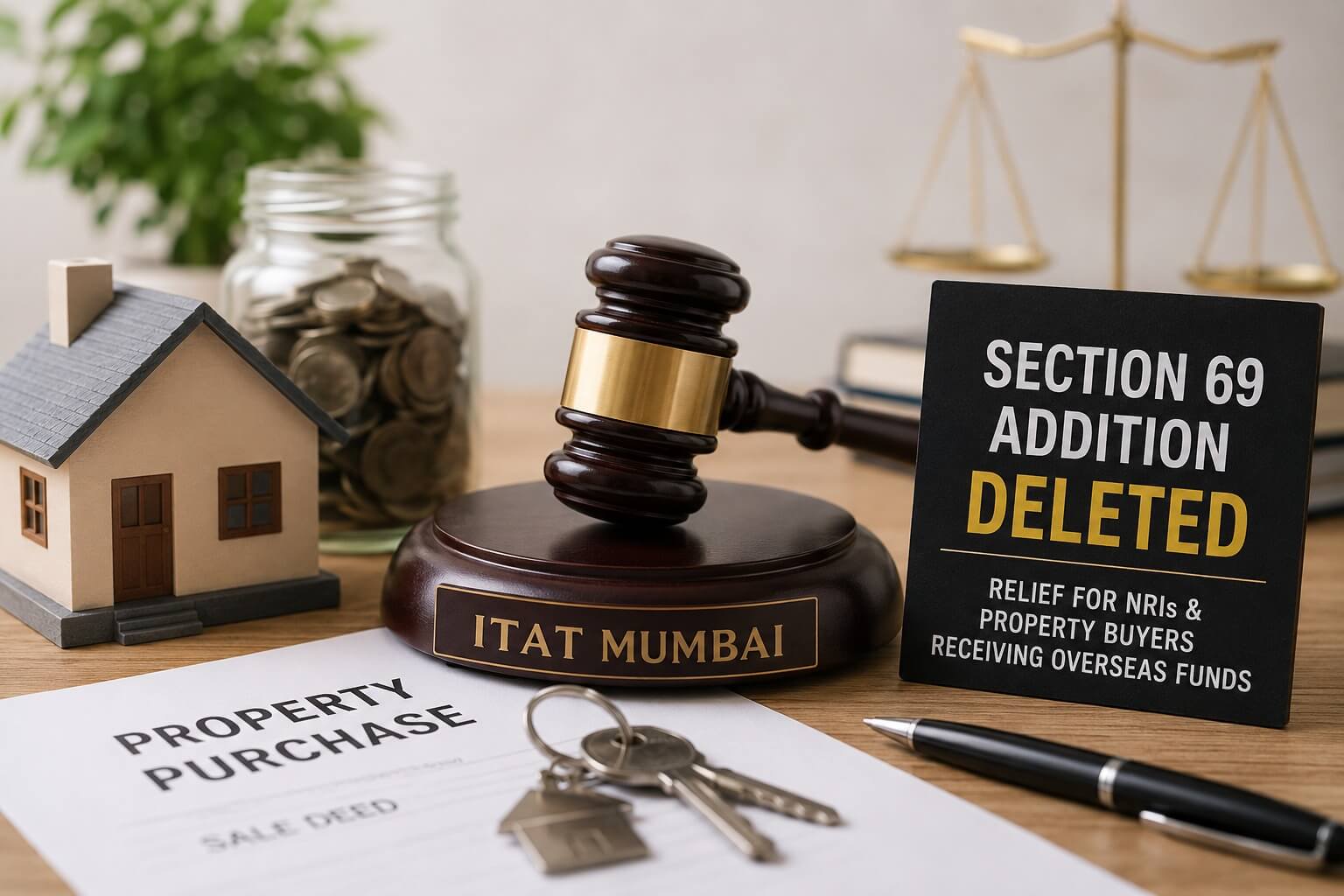

In a significant ruling that will impact NRIs, returning Indians, resident taxpayers receiving funds from relatives abroad, property buyers, and international families, the Income Tax Appellate Tribunal (ITAT), Mumbai has held that an addition under Section 69 of the Income Tax Act cannot be sustained merely because a taxpayer is unable to produce a specific remittance document relating to an old overseas transaction.

The decision in Sanobar Ajaz Ahmed Saudagar vs ITO (ITA No. 1632/Mum/2026) reinforces an important principle of Indian tax law:

When identity, financial capacity, source of funds, and actual utilization of funds are established through credible documentary evidence, the Revenue cannot make additions merely based on suspicion or absence of one historical document.

This ruling is particularly relevant for:

Information regarding the property purchase was available with the Income Tax Department through:

During assessment proceedings, the Assessing Officer examined:

The Assessing Officer accepted part of the source explanation but disputed payments aggregating to ₹80 lakh allegedly made by the taxpayer's husband residing in Dubai directly to the property seller.

Consequently, the department made additions of:

The taxpayer submitted a detailed reconciliation explaining the entire purchase consideration.

Source-wise Breakup of Property Purchase Funds

Table 1

| Particulars | Amount |

| Sale proceeds from earlier property | ₹ 48,00,000 |

| Direct payment by husband from Dubai | ₹ 80,00,000 |

| Gift received from husband | ₹ 20,00,000 |

| Amount utilized from gift | ₹ 18,50,000 |

| Pay order | ₹ 10,000 |

| TDS deducted and deposited | ₹ 1,40,000 |

The taxpayer demonstrated that the entire purchase consideration was fully accounted for.

To substantiate the source of funds, the taxpayer submitted extensive documentary evidence, including:

The documentation established:

The Assessing Officer's primary objection was that the taxpayer could not produce:

Although the seller's bank account reflected credits corresponding to the disputed amount, the department argued that the evidence was insufficient to conclusively prove the source.

The Commissioner of Income Tax (Appeals) agreed with the Assessing Officer and upheld the addition.

The Tribunal had to decide:

The Tribunal observed that:

The husband who funded the property purchase was clearly identified through:

The taxpayer produced sufficient evidence demonstrating the husband's financial capability.

The department did not dispute:

Thus, the creditworthiness requirement stood satisfied.

The seller's bank statements reflected receipt of:

The Tribunal noted that actual receipt by the seller was never disputed.

The Tribunal specifically observed that every component of the purchase consideration was:

There was no unexplained gap in the funding trail.

A crucial aspect of the ruling was that the Revenue failed to establish:

The Tribunal noted that the department merely relied upon absence of one historical document without disproving the taxpayer's explanation.

The Tribunal reiterated a fundamental principle applicable in unexplained investment cases:

This observation has substantial implications for taxpayers facing additions under:

The ruling makes it clear that additions cannot be sustained merely on assumptions when documentary evidence supports the taxpayer's explanation.

This decision has far-reaching implications for non-resident Indians and global Indian families.

Many NRIs purchase property in India using:

This ruling supports taxpayers where historical remittance records may not be readily available.

The judgment is highly relevant where:

The Tribunal recognized that genuine family transactions supported by evidence cannot be disregarded merely due to absence of one document.

A large number of Indians residing in:

utilize exchange houses and remittance channels for transferring money to India.

This ruling acknowledges practical challenges in obtaining decade-old remittance records.

Returning Indians often face scrutiny regarding:

This judgment provides useful support in defending genuine source-of-funds explanations.

Section 69 applies where:

However, courts have consistently held that the taxpayer can discharge the burden by proving:

Identity

Who contributed the funds?

Creditworthiness

Did the contributor have the financial capacity?

Genuineness

Did the transaction actually occur?

Once these elements are established, the burden shifts to the Revenue.

Practical Compliance Lessons for NRIs and Property Buyers

To avoid future disputes, taxpayers should maintain:

The decision strengthens taxpayer defenses in cases involving:

The Tribunal has effectively clarified that tax assessments must be based on evidence rather than suspicion.

Where a taxpayer provides a coherent, documented, and credible explanation supported by surrounding circumstances, the Revenue cannot reject it merely because a single historical record is unavailable.

The ITAT Mumbai ruling in Sanobar Ajaz Ahmed Saudagar vs ITO is an important precedent for NRIs, overseas Indians, property buyers, and taxpayers receiving funds from family members abroad.

The Tribunal recognized that genuine transactions must be evaluated holistically and that tax additions cannot be sustained merely because one piece of historical documentation is unavailable after many years.

For taxpayers involved in international transactions, the ruling provides significant reassurance that courts and tribunals continue to uphold evidence-based assessments and reject additions founded on conjecture or suspicion.

If you have received a notice regarding:

our team at Dinesh Aarjav & Associates specializes in:

CA Dinesh K. Jain is the Founder and Mentor of Dinesh Aarjav & Associates, with over 35 years of experience in NRI taxation, cross-border advisory, project financing, and tax litigation. He has guided numerous NRIs and global families through complex tax and regulatory matters involving investments, repatriation, and international financial planning.

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)