WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

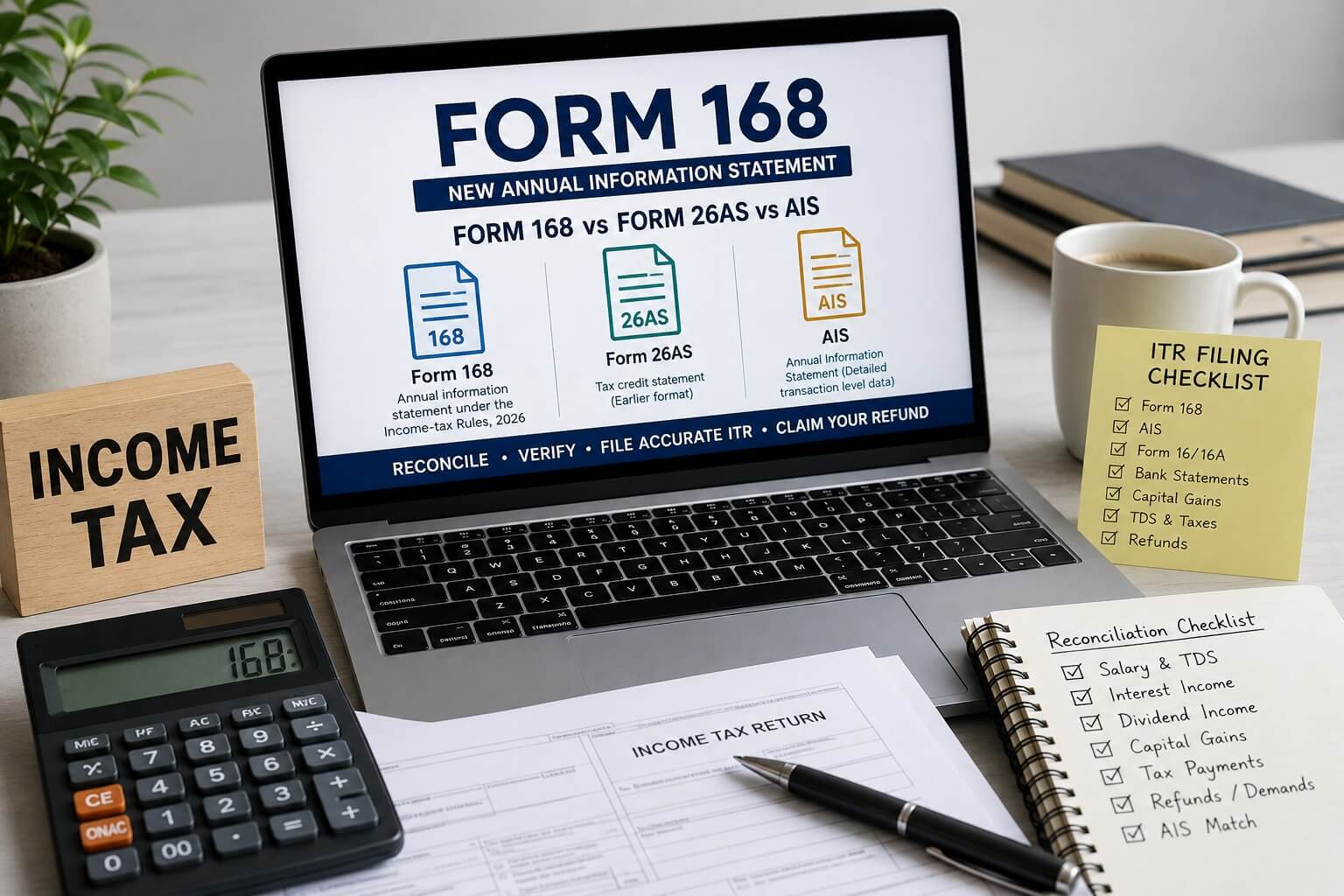

Form 168 is the new annual information statement framework introduced under the Income-tax Act, 2025 and the Income-tax Rules, 2026. It replaces the earlier statutory reference to Form 26AS/AIS and is expected to become an important document for taxpayers filing an income tax return in India. For resident taxpayers, NRIs, returning Indians, salaried professionals, investors, business owners and persons selling property in India, Form 168 can become a key starting point for verifying whether income, tax deductions, tax payments and financial transactions have been correctly reported against their PAN.

Form 168 is relevant because the Income Tax Department increasingly receives information directly from employers, banks, stockbrokers, mutual fund houses, registrars, property registrars, payment platforms and other reporting entities. A taxpayer’s return can therefore be compared with information already available to the department. Filing an ITR without reconciling Form 168, AIS, TIS, Form 16, Form 16A, bank statements and broker reports can lead to tax-credit mismatches, refund delays, compliance notices or requests for clarification.

Form 168 is the annual information statement prescribed under Section 510 of the Income-tax Act, 2025 read with Rule 245 of the Income-tax Rules, 2026. It corresponds to the earlier Form 26AS framework under Section 285BB of the Income-tax Act, 1961 read with Rule 114-I. In simple terms, Form 168 is intended to provide a consolidated view of tax-related and specified financial information linked to a taxpayer’s PAN.

Form 168 may include information relating to:

The precise data visible to a taxpayer will depend on the information reported by third parties and the nature of the taxpayer’s financial activity during the year.

A common question is whether Form 168, Form 26AS and AIS are the same. They are connected, but their role in India income tax return filing is different.

| Document | What It Is | Main Use for ITR Filing |

| Form 168 | New annual information statement framework under the Income-tax Act, 2025 | Review tax credits, tax payments, refunds, demands and reported financial information |

| Form 26AS | Earlier tax-credit statement framework under the Income-tax Act, 1961 | Verify historic TDS, TCS, advance tax, self-assessment tax and refunds |

| AIS | Detailed Annual Information Statement | Review transaction-level reporting from employers, banks, brokers, mutual funds and other reporting entities |

| TIS | Taxpayer Information Summary | Review category-wise totals of salary, interest, dividends, capital gains and taxes paid |

| Form 16 | Salary TDS certificate issued by employer | Verify salary income, deductions, exemptions and TDS |

| Form 16A | Non-salary TDS certificate | Verify TDS on interest, rent, professional fees and other income |

| Bank / Broker Reports | Primary financial records | Compute actual income, taxability, purchase cost, sale value, expenses and capital gains |

Form 168 is the statutory annual information statement framework, AIS provides detailed transaction-wise data, and TIS provides summarized totals. The ITR is still the taxpayer’s final legal declaration. This means taxpayers should not blindly copy figures from AIS, TIS or Form 168 into the ITR. They should use these documents to identify missing income, verify TDS and reconcile discrepancies.

Form 168 represents the new statutory reference under the Income-tax Act, 2025 and the Income-tax Rules, 2026. However, taxpayers should not assume that every Form 26AS reference immediately becomes irrelevant. The applicable statement, portal functionality and reporting format may differ based on the financial year and assessment year involved.

For practical ITR filing, the better question is not “Should I check Form 168 or Form 26AS?” The right question is: “Have I reconciled every tax credit, income item and transaction reflected in the records available for my relevant assessment year?” A taxpayer should review all documents available on the Income Tax e-Filing portal for the relevant year, including Form 168 where applicable, AIS, TIS and tax-credit information.

The Income Tax Department pre-filled ITR data and compliance systems increasingly rely on information reported by third parties. If salary income, interest, dividend income, capital gains, property transactions, foreign remittances or tax credits are visible in Form 168 or AIS but missing from the ITR, the return may attract follow-up communication.

At the same time, Form 168 and AIS are reporting tools—not final tax computations. A bank may report gross interest, while the taxpayer may need to allocate interest in a joint account. A broker may report sale proceeds but may not have the correct acquisition cost, grandfathering value, corporate action adjustments or loss set-off details. A taxpayer may have income that is taxable but not yet reflected in AIS. Therefore, Form 168 should be used as a reconciliation document, not as a substitute for tax computation.

Salaried taxpayers should compare Form 168 and AIS with Form 16 before filing an ITR. The review should cover gross salary, exempt allowances, perquisites, deductions claimed through payroll, professional tax, standard deduction, house-property loss declaration and TDS deducted by the employer.

A salary mismatch may arise because the employer filed a revised TDS return, reported incorrect PAN details, considered a different tax regime, missed a late-year salary component or reported a perquisite differently. The taxpayer should first obtain a revised Form 16 or clarification from the employer. The ITR should be filed using the legally correct salary computation, while ensuring that TDS credit is properly reflected.

Interest income is one of the most frequently missed items in India ITR filing. Taxpayers should reconcile Form 168 and AIS with all savings accounts, fixed deposits, recurring deposits, NRO accounts, NRE accounts, bonds, post-office deposits and other interest-bearing investments.

Banks may report gross interest, while the taxpayer may only see net interest after TDS in the bank account. The ITR must generally report gross interest, with TDS claimed separately as a tax credit. For joint bank accounts, taxpayers should ensure that the interest is reported by the actual beneficial owner and avoid duplicate reporting.

Dividend income should be reconciled with demat account statements, broker reports, registrar and transfer-agent statements, bank credits and mutual fund reports. Taxpayers with multiple brokers or family holdings should carefully verify whether an AIS entry belongs to them and whether it has been reported more than once.

Capital gains are often the most complex part of Form 168 and AIS reconciliation. A stockbroker or mutual fund platform may report sale transactions, but its data may not fully capture the taxpayer’s correct cost of acquisition, brokerage, Securities Transaction Tax treatment, bonus shares, stock splits, rights issues, corporate mergers, grandfathering benefit, carry-forward losses or set-off of current-year losses.

Taxpayers should calculate capital gains using transaction-level broker reports, contract notes, mutual fund capital-gains statements and their own investment records. This is especially important for taxpayers who have sold listed shares, unlisted shares, ESOP shares, mutual funds, property, cryptocurrency or other capital assets.

For property sales, the seller should reconcile sale consideration, TDS deducted by the buyer, lower-TDS certificate details where applicable, stamp-duty value, purchase cost, improvement cost, exemption claims and capital-gains deposit account details. NRIs selling property in India should take particular care because property-sale TDS, capital-gains computation and refund claims can be significant.

Form 168 can be particularly useful for NRIs filing an India income tax return. NRIs may have India-source income from NRO bank accounts, fixed deposits, rental income, dividends, mutual funds, shares, property sales, pension, consultancy income or interest-bearing investments. Tax may be deducted at source at higher rates, and a return may be required to claim a refund, report capital gains, carry forward losses or apply treaty relief where eligible.

NRIs should reconcile Form 168 and AIS with NRO bank statements, NRE account records, property-sale documents, Form 16A, broker reports and foreign tax records. They should also evaluate whether their residential status, tax treaty position, foreign tax credit claim, lower-TDS certificate, Form 10F and Tax Residency Certificate requirements have been correctly addressed.

For returning Indians and RNOR taxpayers, Form 168 is useful but does not decide tax residency. Residential status must be separately determined based on the taxpayer’s physical presence in India and other applicable conditions. The scope of taxable foreign income may differ for a resident, RNOR and non-resident taxpayer.

A mismatch does not automatically mean that the taxpayer has under-reported income. It may result from a reporting delay, incorrect PAN, duplicate reporting, incorrect source reporting, joint ownership, a gross-versus-net difference, an incorrect classification or a transaction that does not belong to the taxpayer.

Taxpayers should first prepare a reconciliation statement. This should compare the entry appearing in Form 168 or AIS with the corresponding Form 16, Form 16A, bank statement, broker report, contract note, challan or other supporting document. The reconciliation should record the final ITR figure and explain the reason for any difference.

If an AIS entry is incorrect, duplicated or unrelated, feedback should be submitted through the AIS portal. TIS cannot be directly edited; it is updated after AIS feedback is processed. If TDS is missing or incorrect, taxpayers should request the employer, bank, tenant, buyer, client or other deductor to revise the TDS return. If the mismatch relates to a broker, mutual fund house or bank, the taxpayer should request corrected records and preserve correspondence.

Before filing your income tax return in India, complete the following review:

Taxpayers often lose time and face delayed refunds because of avoidable errors. Common mistakes include claiming TDS that does not appear in the tax-credit statement, reporting net bank interest instead of gross interest, missing interest from inactive bank accounts, omitting dividend income, using broker-reported capital gains without checking cost of acquisition, ignoring AIS feedback, reporting incorrect residential status, failing to disclose foreign assets where applicable and filing the wrong ITR form.

Another frequent error is assuming that “not shown in AIS” means “not taxable.” This is incorrect. Taxpayers are required to report all taxable income, even if it is not visible in Form 168, AIS or TIS.

Taxpayers can access AIS and TIS by logging in to the Income Tax e-Filing portal and navigating to the AIS section under the Income Tax Returns or Compliance Portal area. The portal may display Form 168 or the applicable annual information statement depending on the relevant financial year and the ongoing transition framework. Download the PDF and JSON versions where available, and preserve them with your tax records.

A pre-filled ITR is not necessarily a correct ITR. Form 168, AIS and TIS are excellent tools for identifying reportable information, but they cannot independently determine whether income is exempt, whether capital gains have been computed correctly, whether losses can be set off, whether DTAA relief is available or whether foreign-asset disclosures apply.

Professional review is particularly useful where the taxpayer has multiple income sources, investments, property transactions, NRI status, foreign income, ESOPs, stock options, cryptocurrency transactions, business income, rental income, capital losses or refund claims.

Dinesh Aarjav & Associates helps resident taxpayers, NRIs, OCI cardholders, returning Indians, salaried professionals, founders and investors with India income tax return filing, Form 168 reconciliation, AIS and TIS review, TDS refund claims, capital-gains computation, property-sale taxation, DTAA support and cross-border tax compliance.

Our India tax filing support can help you:

CA Nitin Jain is an Associate at Dinesh Aarjav & Associates with more than 10 years of experience specializing in NRI taxation, cross-border tax matters, assessments, appeals, and tax litigation. He regularly assists NRIs and international clients in navigating Indian tax compliance requirements and representing them before various tax authorities.

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)