WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

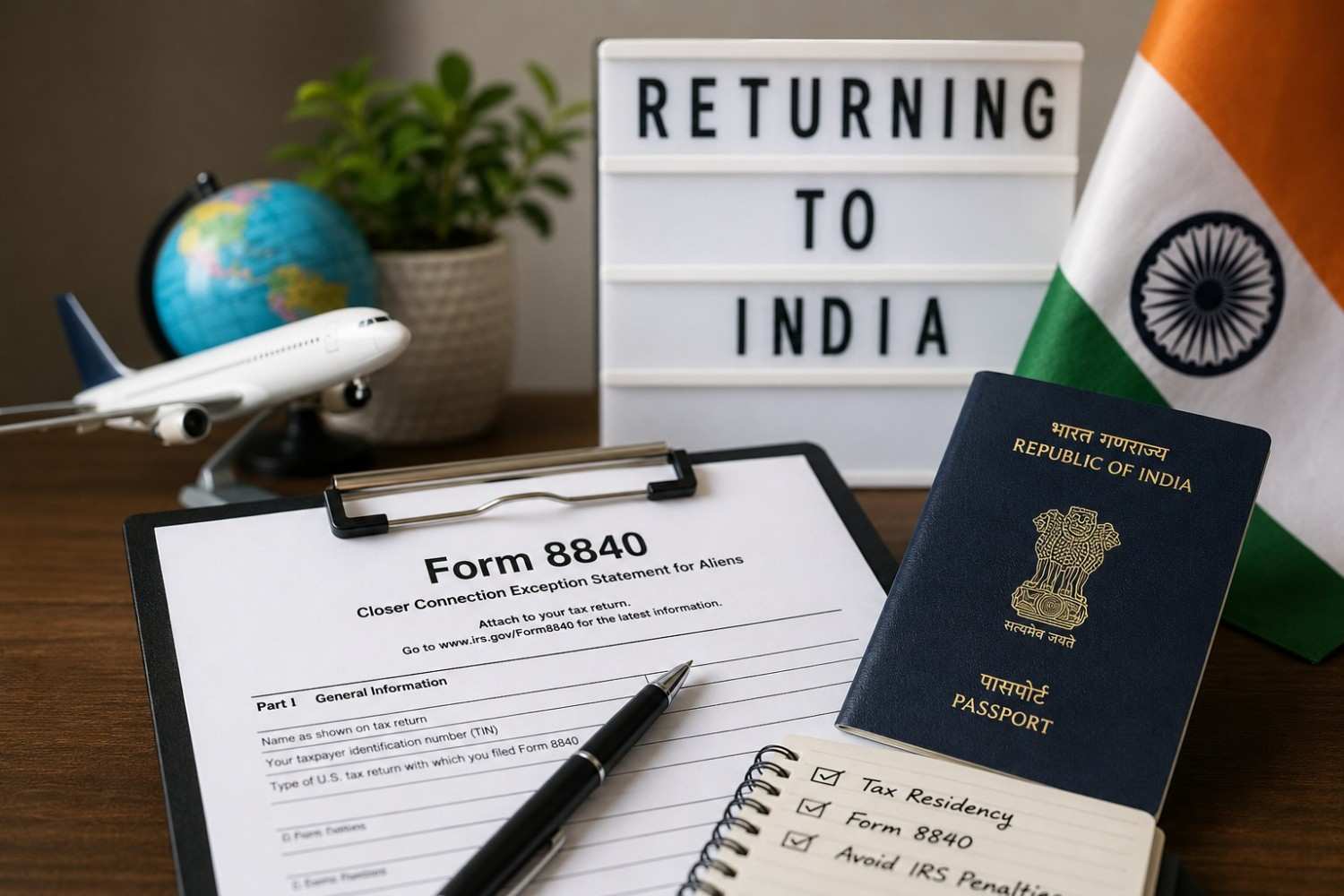

Returning to India from the United States? One overlooked tax filing could expose your Indian income and investments to unnecessary US tax complications.

For Indians moving back to India after living in the US, filing Form 8840 (Closer Connection Exception Statement for Aliens) and a Residency Termination Statement can be a critical step in ending US tax residency correctly.

Many returning Indians assume that simply leaving the US automatically ends their US tax obligations. However, in many situations, the IRS may continue to treat you as a US tax resident unless the appropriate filings are completed.

In this guide, we explain why Form 8840 matters, who should file it, how the Closer Connection Exception works, and the risks of missing this compliance requirement.

When an individual leaves the United States and intends to end US tax residency, Treasury Regulations under 26 CFR § 301.7701(b)-8 require a residency termination statement to be submitted with the final US tax filing (typically Form 1040-NR). This helps establish the date on which US tax residency ended.

For many Indians returning from the US, Form 8840 becomes equally important because it allows an individual to claim the Closer Connection Exception, helping demonstrate that their tax home and closer connection are outside the United States.

Failing to complete these filings can create unnecessary tax uncertainty at a time when you are transitioning your finances back to India.

If Form 8840 and the residency termination statement are not properly filed, there may be a risk that the IRS treats you as a US tax resident for the entire calendar year.

This can lead to consequences such as:

1. Taxation on Worldwide Income

Your income earned after returning to India, including Indian salary, investment income, rental income, and foreign earnings, could potentially become subject to US tax reporting.

2. Indian and Non-US Investments Coming Under US Tax Scope

Investments made after returning to India may still fall under US tax jurisdiction if tax residency is not properly terminated.

3. Double Taxation and Compliance Complexity

Incorrect residency treatment may result in overlapping tax obligations across countries, creating avoidable compliance burdens and financial uncertainty.

Form 8840 is used to claim the “Closer Connection Exception” to the Substantial Presence Test (SPT). It helps establish that, although you may otherwise satisfy US physical presence requirements, your stronger economic and personal connection lies outside the United States.

For Indians returning home, this filing can help support the position that India—not the US—is your primary tax jurisdiction.

The IRS uses the Substantial Presence Test (SPT) to determine whether a non-US citizen may be treated as a US tax resident based on physical presence in the country.

However, the 183-day formula is not the complete picture.

Several important nuances, exclusions, and exceptions apply, making proper tax evaluation critical for Indians relocating back to India.

Even if the weighted 183-day Substantial Presence Test is met, an individual may still be treated as a non-resident of the US by claiming the Closer Connection Exception under Form 8840.

To qualify, ALL of the following conditions must generally be satisfied:

1. You Were Present in the US for Fewer Than 183 Days

You must have been physically present in the United States for less than 183 days during the relevant calendar year.

2. You Had a Tax Home in a Foreign Country

You must establish that your tax home existed outside the United States.

Generally:

3. You Had a Closer Connection to a Foreign Country Than the US

You must establish that your contacts with the foreign country are more significant than those with the United States.

The IRS may evaluate factors such as:

4. Form 8840 Must Be Filed

The benefit of the closer connection exception generally depends upon timely filing Form 8840 with the IRS.

5. You Should Not Have Applied for a Green Card

Individuals who are green card holders or have applied for one are generally not eligible to claim this exception.

Many professionals returning from the US begin:

If US tax residency is not properly addressed, these post-return financial activities could become entangled in unnecessary US tax reporting concerns. Proper filings can help establish clarity regarding your tax position.

To reduce tax complications during relocation back to India, individuals should generally consider:

Filing Form 1040-NR with a Residency Termination Statement

This helps indicate the end of US residency for tax purposes.

Filing Form 8840

Where eligible, this may help establish a closer connection outside the United States.

Reviewing Cross-Border Tax Position

A proper review of residency, investments, and future reporting obligations can help avoid avoidable tax issues after moving back to India.

Properly resolving US tax matters may help avoid future compliance concerns and support smoother travel or re-entry situations from a documentation perspective. As every case differs, tax and immigration matters should be evaluated separately.

At Dinesh Aarjav & Associates, we assist NRIs, returning Indians, expatriates, and globally mobile families with complex India-US cross-border tax matters.

With 25+ years of experience, offices across multiple countries, and 2,600+ domestic and international clients, our team assists with:

If you are returning from the United States, getting your tax residency position right from the beginning can help avoid costly issues later.

Returning to India from the US is not just a relocation—it is also a tax transition.

Many Indians overlook the importance of properly ending US tax residency, only to face complications later. Filing Form 8840 and a residency termination statement, where applicable, may help establish clarity and reduce avoidable tax uncertainty.

If you are planning your move back to India or have already returned, seeking timely guidance can make your transition significantly smoother.

RSU Taxation in the UK for NRIs: Complete Guide to Filing, Double Taxation Relief & Deadlines

CA Tripti Goel, EA and Chartered Accountant, specializes in India–US cross-border taxation, NRI tax advisory, US tax compliance, and international financial reporting. With extensive experience across multinational organizations, she advises clients on US tax matters, cross-border income reporting, and tax-efficient financial planning for NRIs.

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)