WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

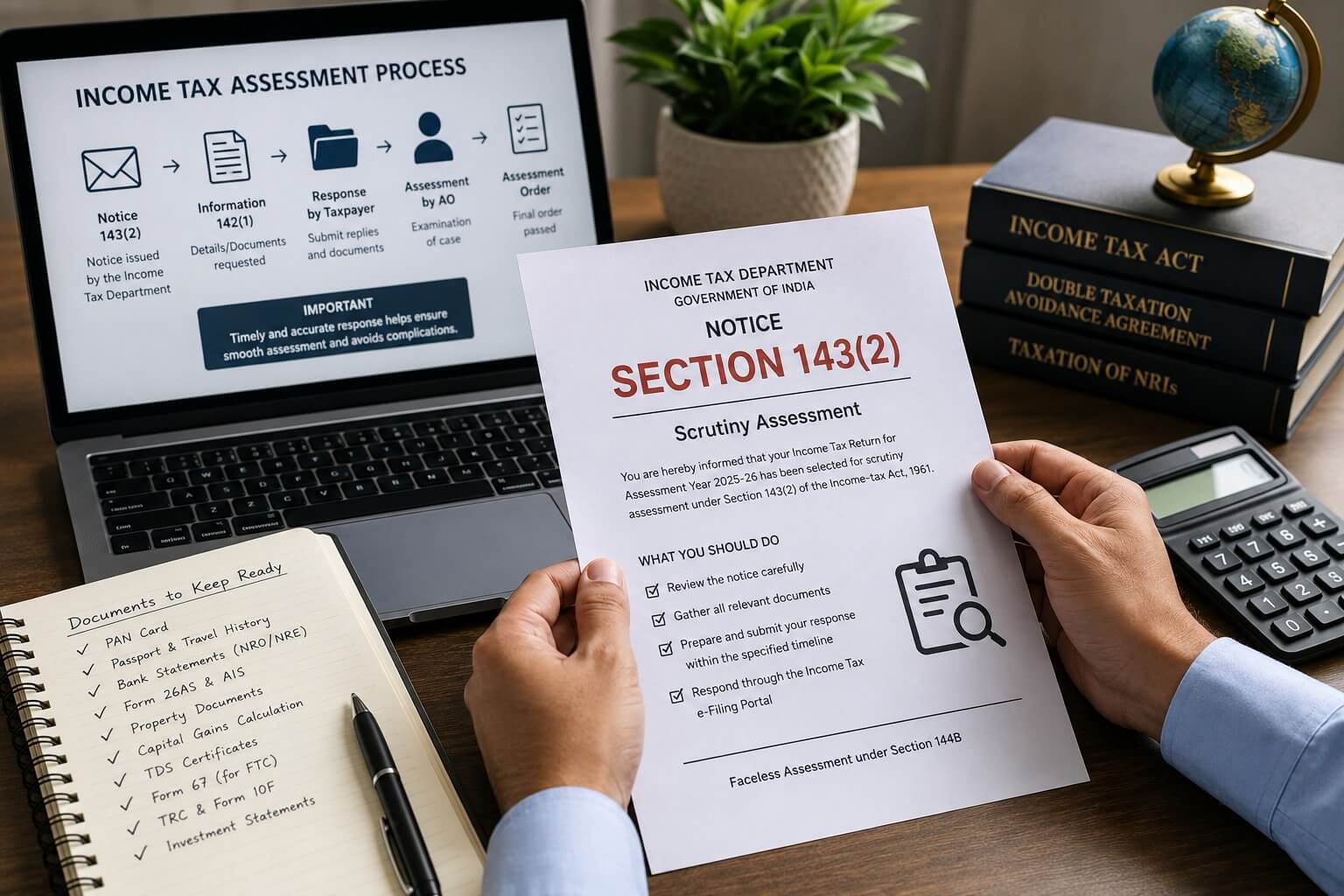

As the Income Tax Return (ITR) filing season for Assessment Year (AY) 2026–27 progresses, many taxpayers have recently received Section 143(2) notices from the Income Tax Department in relation to returns filed for AY 2025–26. While receiving such a notice may seem alarming, it is important to understand that a scrutiny notice does not automatically imply tax evasion, concealment of income, or any wrongdoing. It simply means that the Income Tax Department has selected your return for a detailed verification.

For Non-Resident Indians (NRIs), Overseas Citizens of India (OCIs), Returning Indians (RNORs), expatriates, and individuals with cross-border financial transactions, scrutiny assessments have become increasingly common due to the complexity of international tax reporting and the extensive use of technology by the Income Tax Department.

If your return involves the sale of property in India, capital gains, Double Taxation Avoidance Agreement (DTAA) benefits, Foreign Tax Credit (FTC), NRO/NRE accounts, overseas income, or significant refund claims, understanding the scrutiny process and responding appropriately becomes even more important.

A notice under Section 143(2) of the Income-tax Act, 1961 (corresponding to Section 270 of the Income-tax Act, 2025) is issued when the Income Tax Department selects a return for scrutiny assessment.

The purpose of scrutiny is to verify whether:

A scrutiny notice is therefore a verification mechanism and not a conclusion that additional tax is payable.

This is one of the most common questions taxpayers ask.

Many taxpayers assume that once an Income Tax Return has been processed under Section 143(1), the matter is closed. However, processing under Section 143(1) is only an automated preliminary check.

Even after your return has been processed or your refund has been issued, the Income Tax Department may subsequently select your return for scrutiny assessment under Section 143(2) if it considers further verification necessary. Therefore, receiving a scrutiny notice after processing is perfectly valid and does not, by itself, indicate any discrepancy.

Compared to resident taxpayers, NRIs often have more complex financial affairs spanning multiple jurisdictions. Consequently, their returns may receive greater attention during risk assessment.

Some common reasons include:

The department may verify:

Where foreign taxes have been claimed as credit in India, the department may seek verification of:

Transactions commonly selected for verification include:

The Income Tax Department increasingly relies on information available in:

Any mismatch between these records and the Income Tax Return may trigger scrutiny.

An incorrect determination of residential status can significantly impact taxation of global income, DTAA eligibility and disclosure requirements. Residential status remains one of the most scrutinised aspects of NRI taxation.

The Income Tax Department now uses advanced data analytics, artificial intelligence, risk management systems and information received from various reporting entities to identify returns requiring closer examination.

Returns may be selected based on:

Many taxpayers become anxious because the Section 143(2) notice itself often does not specify the exact issue under scrutiny.

This is entirely normal.

The notice merely informs you that your return has been selected for scrutiny. The detailed information, explanations or documents required are generally sought later through a Section 142(1) notice, which forms part of the assessment proceedings.

Many taxpayers receiving a scrutiny notice also receive an intimation under Section 144B.

This relates to the Faceless Assessment Scheme, under which most scrutiny assessments are conducted electronically through the Income Tax e-Filing Portal.

Taxpayers generally do not need to visit the Income Tax Department physically. Notices, replies, supporting documents and communications are exchanged online, making the assessment process more transparent and efficient.

Depending upon the issues involved, the Income Tax Department may request:

Maintaining organised records significantly improves the quality of your response during assessment proceedings.

A systematic response can substantially improve the outcome of scrutiny proceedings.

The assessment process generally follows these stages:

For complex NRI matters involving property sales, DTAA, Foreign Tax Credit or overseas income, multiple rounds of clarification may be required before the assessment is concluded.

Ignoring an Income Tax notice can have significant consequences.

These may include:

Timely and well-supported responses are therefore essential.

Sometimes taxpayers realise during assessment proceedings that an income item has been omitted or a deduction has been incorrectly claimed.

Depending upon the facts and the applicable legal provisions, appropriate corrective action may still be possible. Seeking professional advice at an early stage can often help minimise disputes and ensure compliance with tax laws. In some cases, statutory relief provisions may also be available where conditions are satisfied.

Responding to an Income Tax notice requires much more than uploading documents. Effective representation involves analysing the legal issues, preparing technically sound submissions, supporting them with documentary evidence and ensuring timely compliance throughout the assessment process.

At Dinesh Aarjav & Associates, we provide comprehensive advisory and representation services for individuals, NRIs, Returning Indians, expatriates and businesses in relation to assessments and notices under both the Income-tax Act, 2025 and the Income-tax Act, 1961.

Our services include:

Our Chartered Accountants regularly assist clients across the United States, Canada, the United Kingdom, Australia, the UAE, Singapore and several other jurisdictions, providing practical solutions for complex Indian and cross-border tax matters.

A Section 143(2) Income Tax Notice should be viewed as an opportunity to substantiate the information disclosed in your Income Tax Return rather than as an indication of wrongdoing. Responding with complete documentation, accurate explanations and within the prescribed timelines is essential for a smooth assessment process.

If you have received an Income Tax notice, require assistance with scrutiny assessments, reassessment proceedings, rectification applications, appeals, or need professional representation before the Income Tax Department, Dinesh Aarjav & Associates can provide end-to-end support to help you navigate the assessment process with confidence.

Aarjav Jain is the Executive Director at Dinesh Aarjav & Associates, specializing in India–US cross-border transactions, NRI taxation, international tax advisory, and global investment structuring. With over 10 years of experience in project financing and cross-border advisory, he assists NRIs and businesses with regulatory compliance, repatriation planning, and international transaction structuring.

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)