WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

Indian Fixed Deposits (FDs) continue to be one of the most preferred investment options for NRIs due to their safety, predictable returns, and attractive interest rates. However, if you are a US Citizen, Green Card holder, H-1B visa holder, Resident Alien, or otherwise a US tax resident, you may have reporting and tax obligations in the United States—even if your Fixed Deposit is held with an Indian bank.

One of the most common misconceptions is that if an NRE Fixed Deposit is tax-free in India, it is also tax-free in the United States. Unfortunately, that is not the case.

The IRS taxes US tax residents on their worldwide income, which generally includes interest earned from Indian Fixed Deposits. Depending on your investments, you may also have to comply with FBAR, FATCA (Form 8938) and other international reporting requirements.

This guide explains how NRE, NRO and FCNR Fixed Deposits are taxed in the USA, the reporting requirements, and how the India-US DTAA can help reduce double taxation.

Yes. If you are considered a US tax resident, interest earned from Indian Fixed Deposits is generally taxable in the United States, irrespective of whether the interest is taxable or exempt in India.

The IRS follows the principle of worldwide taxation, which means foreign interest income must generally be reported on your US tax return.

NRIs typically invest in three types of Fixed Deposits:

| Fixed Deposit | Tax Treatment in India | Tax Treatment in the USA |

| NRE Fixed Deposit | Interest is generally exempt from tax in India (subject to applicable conditions) | Interest is generally taxable in the USA |

| NRO Fixed Deposit | Interest is taxable in India and may be subject to TDS | Interest is generally taxable in the USA |

| FCNR Fixed Deposit | Interest is generally exempt from tax in India (subject to applicable conditions) | Interest is generally taxable in the USA |

While Indian tax laws provide exemptions for certain deposits, the IRS does not distinguish between NRE, NRO and FCNR deposits for determining whether the interest is taxable. If you are a US tax resident, the interest generally forms part of your taxable income.

Unlike many countries, the United States taxes its tax residents on their global income, regardless of where the income is earned.

This means the following income may need to be reported in the US:

Simply because the income is earned in India does not mean it is exempt from US taxation.

Another area of confusion is when the interest becomes taxable.

Many investors assume they only need to report interest when the Fixed Deposit matures. However, depending on the nature of the deposit and the applicable US tax rules, interest may need to be reported as it accrues, even if it has not been withdrawn or credited to your savings account.

This is particularly important for long-term Fixed Deposits where the interest is reinvested until maturity.

Proper tax reporting ensures you avoid under-reporting income and potential IRS notices.

Yes.

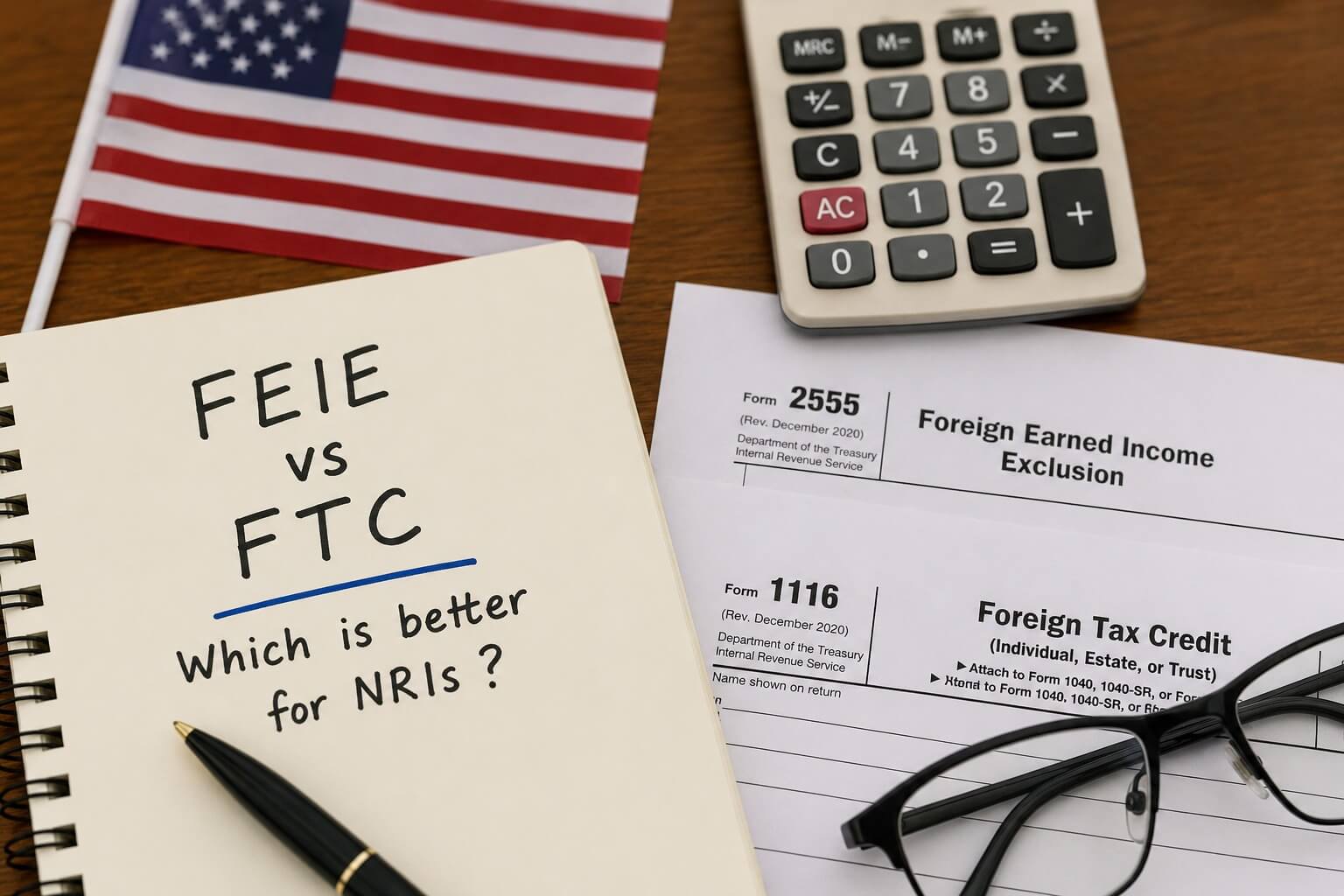

If tax has already been deducted in India—such as TDS on an NRO Fixed Deposit—you may be eligible to claim a Foreign Tax Credit (FTC) in your US tax return, subject to the applicable rules.

The India-US Double Taxation Avoidance Agreement (DTAA) and the Foreign Tax Credit provisions are designed to reduce the possibility of paying tax twice on the same income.

Maintaining tax deduction certificates and other supporting documents is important when claiming these benefits.

Taxation is only one part of the compliance requirements.

Depending on your circumstances, Indian Fixed Deposits and the bank accounts in which they are held may also trigger international reporting obligations.

If the aggregate value of all your foreign financial accounts exceeds USD 10,000 at any time during the calendar year, you may be required to file an FBAR.

Many taxpayers overlook Indian bank accounts and Fixed Deposits while calculating this threshold, leading to avoidable penalties.

Certain US taxpayers must also disclose specified foreign financial assets under FATCA by filing Form 8938, if the applicable reporting thresholds are exceeded.

Whether Form 8938 is required depends on factors such as your filing status, residency, and the total value of your foreign assets.

Example

Rahul is a Green Card holder living in New Jersey. He has the following investments in India:

Although the interest on his NRE and FCNR deposits may be exempt from tax in India, he generally needs to report the interest earned on all his Fixed Deposits in his US tax return. If tax has been deducted on the NRO Fixed Deposit, he may also be able to claim a Foreign Tax Credit, subject to eligibility.

In addition, if the combined value of his foreign financial accounts exceeds the prescribed limits, he may also have FBAR and FATCA reporting obligations.

Some of the most common mistakes include:

These errors can result in unnecessary tax exposure, interest, or penalties.

Cross-border taxation of Indian investments requires careful planning. Apart from reporting interest income, taxpayers also need to consider Foreign Tax Credit claims, FBAR, FATCA, and other international reporting requirements.

At Dinesh Aarjav & Associates, our cross-border tax specialists assist NRIs with:

Indian Fixed Deposits remain a popular investment option for NRIs, but they can also create US tax and reporting obligations. Whether you hold NRE, NRO or FCNR Fixed Deposits, understanding how the IRS taxes foreign interest income is essential for staying compliant.

With timely reporting, proper documentation, and effective use of the India-US DTAA and Foreign Tax Credit, you can minimise the risk of double taxation while meeting your compliance obligations in both countries.

If you hold Indian Fixed Deposits and are unsure about your US tax responsibilities, seeking professional cross-border tax advice can help you avoid costly mistakes and ensure accurate reporting.

CA Sanyam Goel, CPA (USA), FCA, and CISA, specializes in India–US cross-border taxation, NRI tax advisory, US tax compliance, transfer pricing, and international regulatory matters. He assists clients with US and Indian tax obligations, cross-border reporting requirements, and strategic tax planning for global investments and transactions.

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)