WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

For Non-Resident Indians (NRIs), Overseas Citizens of India (OCI Card Holders), and Returning Indians, filing an Income Tax Return (ITR) in India has become significantly more technical than simply reporting Indian income.

With the introduction of the Income Tax Act, 2025, taxpayers with cross-border financial interests must carefully determine their residential status, select the correct ITR form, claim eligible treaty benefits, disclose foreign income where applicable, and comply with additional reporting requirements such as Form 67, Form 10EE, Schedule FSI, and Schedule FA.

The Income Tax Department has also issued guidance for Non-Resident Individuals for AY 2026-27, helping taxpayers identify the applicable ITR forms and related compliances before filing their return.

Whether you are:

filing your Indian Income Tax Return correctly is essential to avoid double taxation, claim refunds, and remain fully compliant.

At Dinesh Aarjav & Associates, we specialise in NRI Taxation, International Tax Advisory, Returning to India Planning and Cross-Border Tax Compliance, assisting clients across more than 40 countries.

Many NRIs believe that because tax has already been deducted at source (TDS), they do not need to file an Income Tax Return in India.

This is one of the biggest misconceptions.

An Indian Income Tax Return is often necessary to:

A properly filed return not only ensures compliance but also helps optimise your overall tax position.

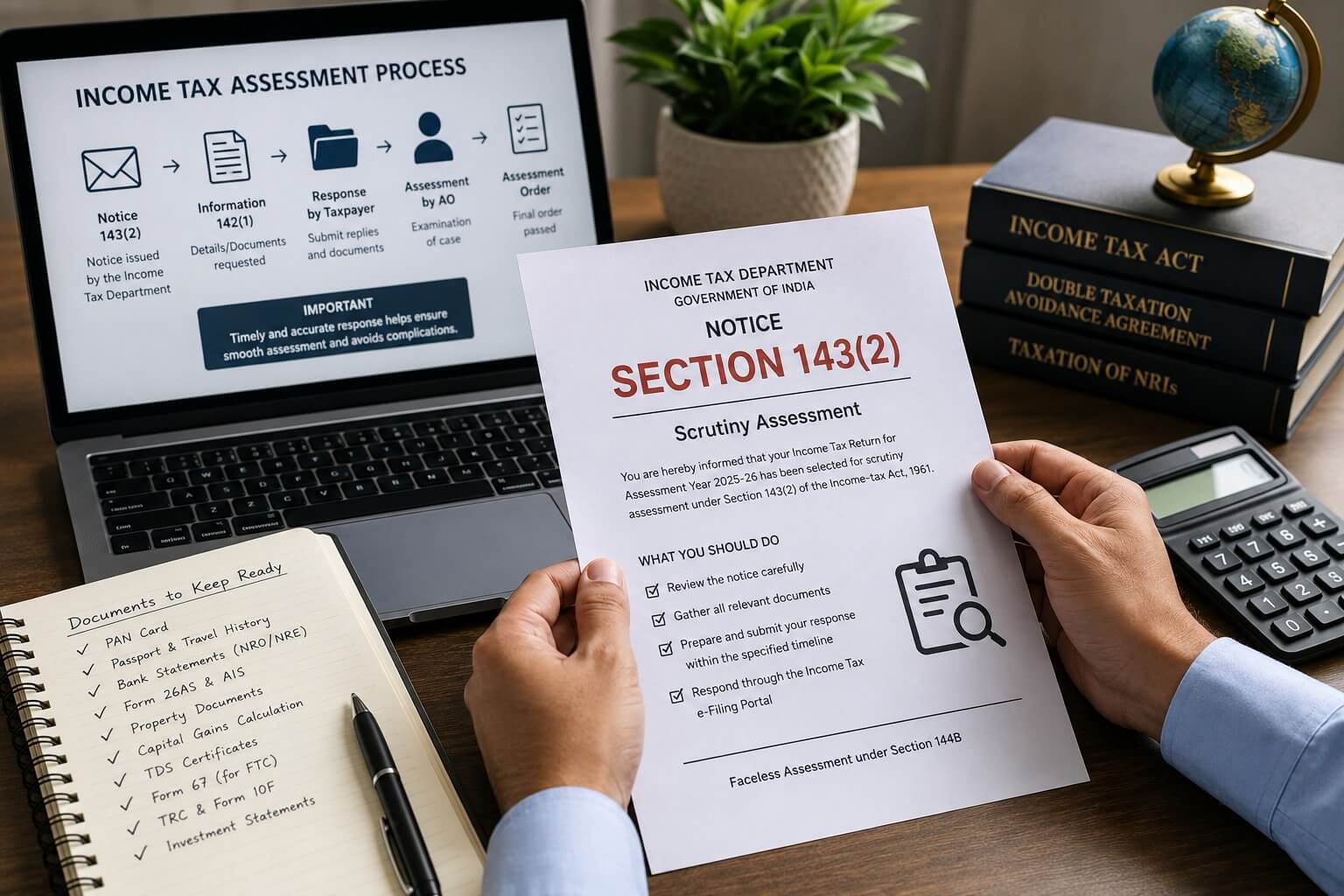

Step 1 – Determine Your Residential Status

Before selecting an ITR form, every taxpayer should first determine their residential status under the Income Tax Act.

Your status could be:

This determination affects:

For Returning Indians, determining residential status correctly is often the most important tax planning exercise of the year.

The Income Tax Department's guidance for AY 2026-27 explains that the applicable ITR depends on the taxpayer's residential status and nature of income.

NRIs commonly file:

ITR-2

Applicable where income generally consists of:

and there is no business or professional income.

ITR-3

Applicable where the taxpayer has:

Selecting the wrong return may delay refunds or result in the return being treated as defective.

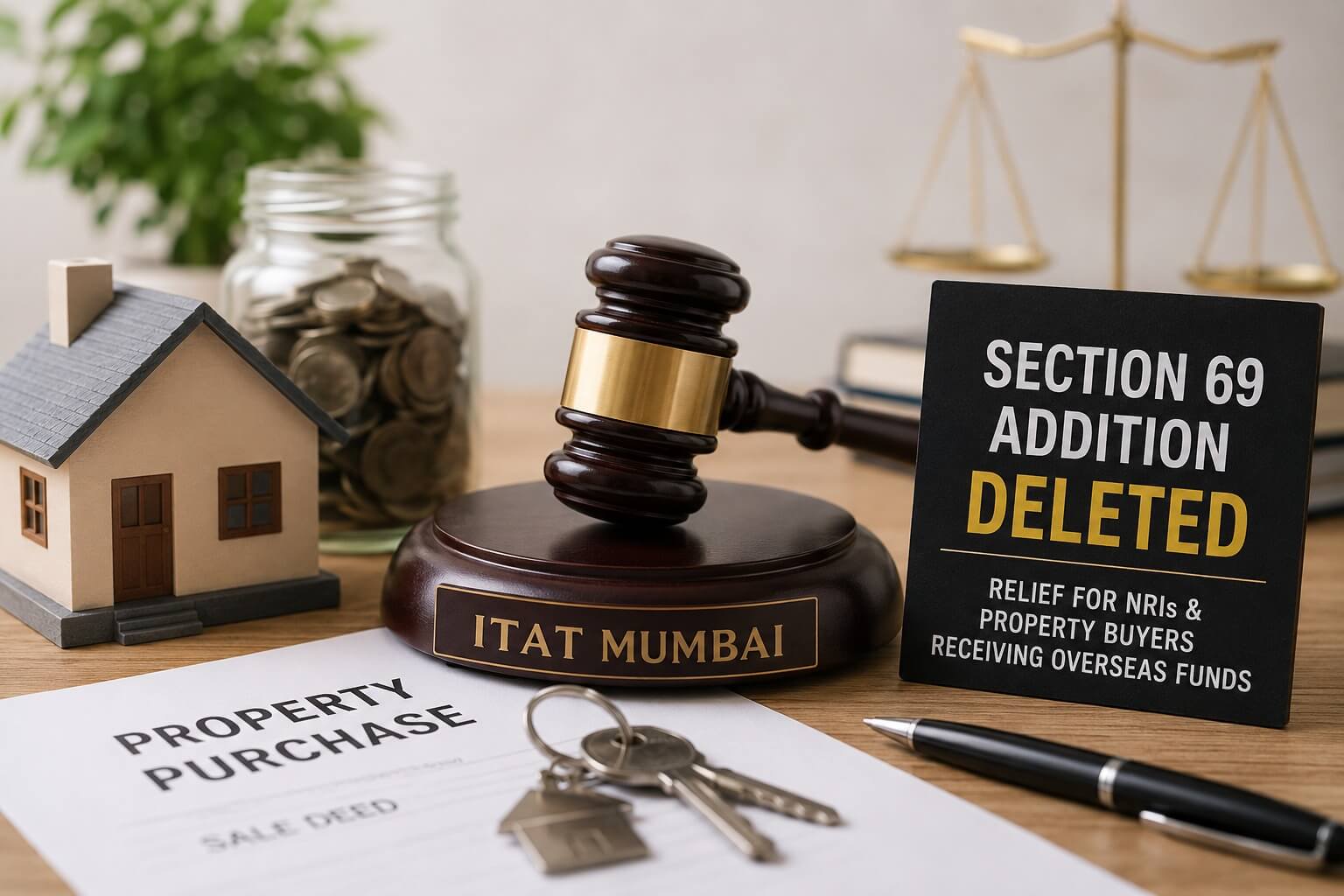

Many overseas Indians are surprised to learn that even limited Indian income may require filing an Income Tax Return.

Common examples include:

Even where TDS has already been deducted, filing an ITR may still be necessary to determine the correct tax liability and claim refunds.

Moving back to India is not merely a change of address—it is a change in your tax profile.

Returning NRIs often transition through:

Each stage has different implications for:

The RNOR period can provide valuable tax planning opportunities if structured correctly before relocating to India.

Unfortunately, many taxpayers lose these opportunities simply because they seek tax advice after becoming residents.

One of the fastest-growing areas of international taxation involves Restricted Stock Units (RSUs), Employee Stock Options (ESOPs), Performance Shares and other equity compensation.

Professionals working with multinational companies frequently receive compensation through stock awards.

If you have worked with organisations such as:

your tax reporting may involve both Indian and overseas tax laws.

Issues commonly arise regarding:

Incorrect reporting of RSUs is one of the most common reasons for double taxation among globally mobile professionals.

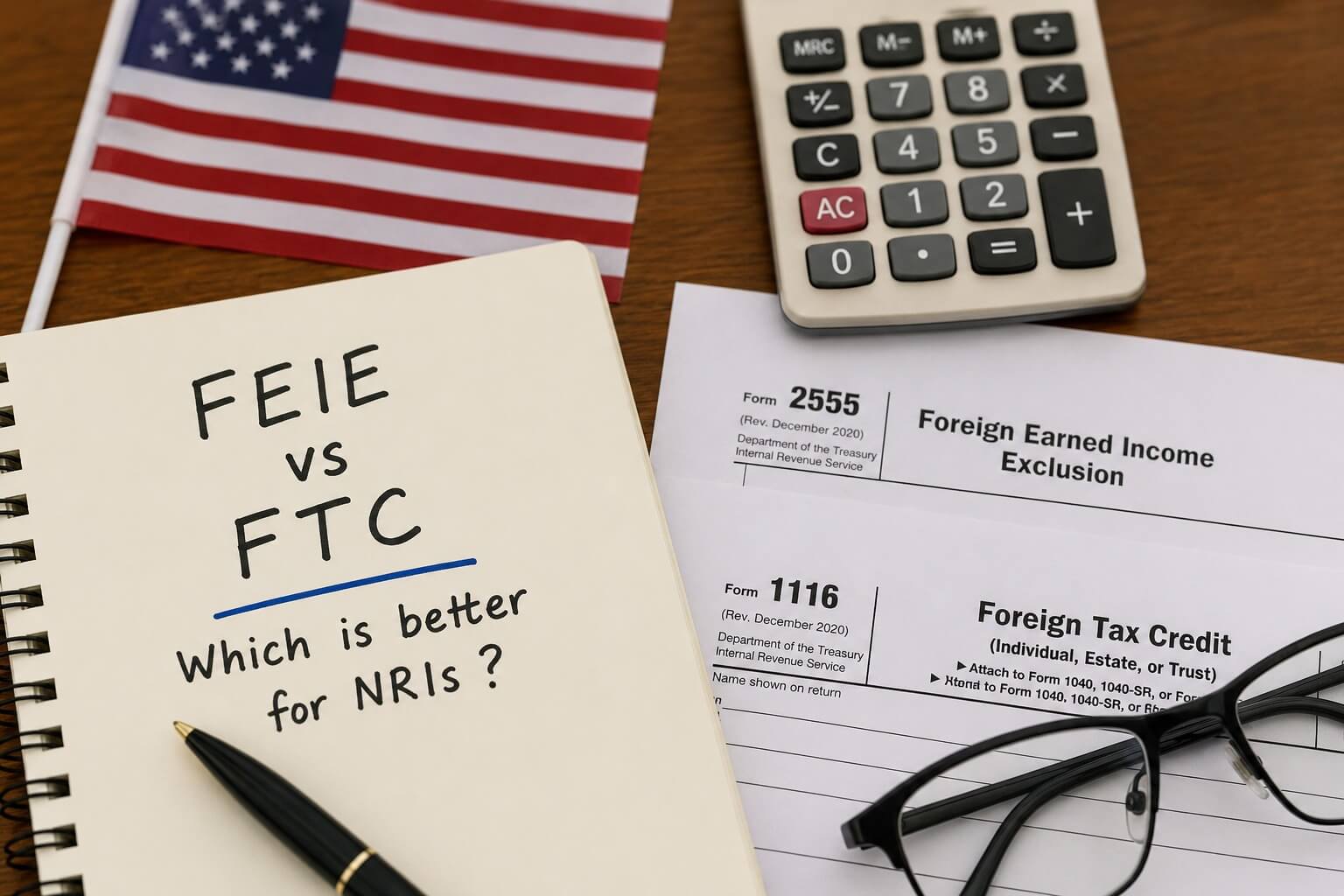

If tax has already been paid outside India, it does not necessarily mean the same income should be taxed again.

India has entered into Double Taxation Avoidance Agreements (DTAAs) with several countries to prevent double taxation.

Examples include:

To claim Foreign Tax Credit correctly:

Common situations include:

Failure to comply with procedural requirements may affect the availability of Foreign Tax Credit.

Many NRIs maintain retirement accounts overseas even after relocating to India.

These may include:

For eligible taxpayers, Form 10EE continues to facilitate relief relating to specified foreign retirement accounts under the applicable provisions.

Proper reporting is essential to avoid unintended taxation.

Foreign income taxable in India may need to be disclosed under Schedule FSI.

Typical disclosures include:

Schedule FSI works closely with Foreign Tax Credit computations and Form 67.

Incorrect reporting frequently results in mismatches and delayed processing.

Returning Indians often underestimate their reporting obligations.

Depending upon residential status, Schedule FA may require disclosure of:

These disclosures should be made carefully and consistently with the taxpayer's financial records.

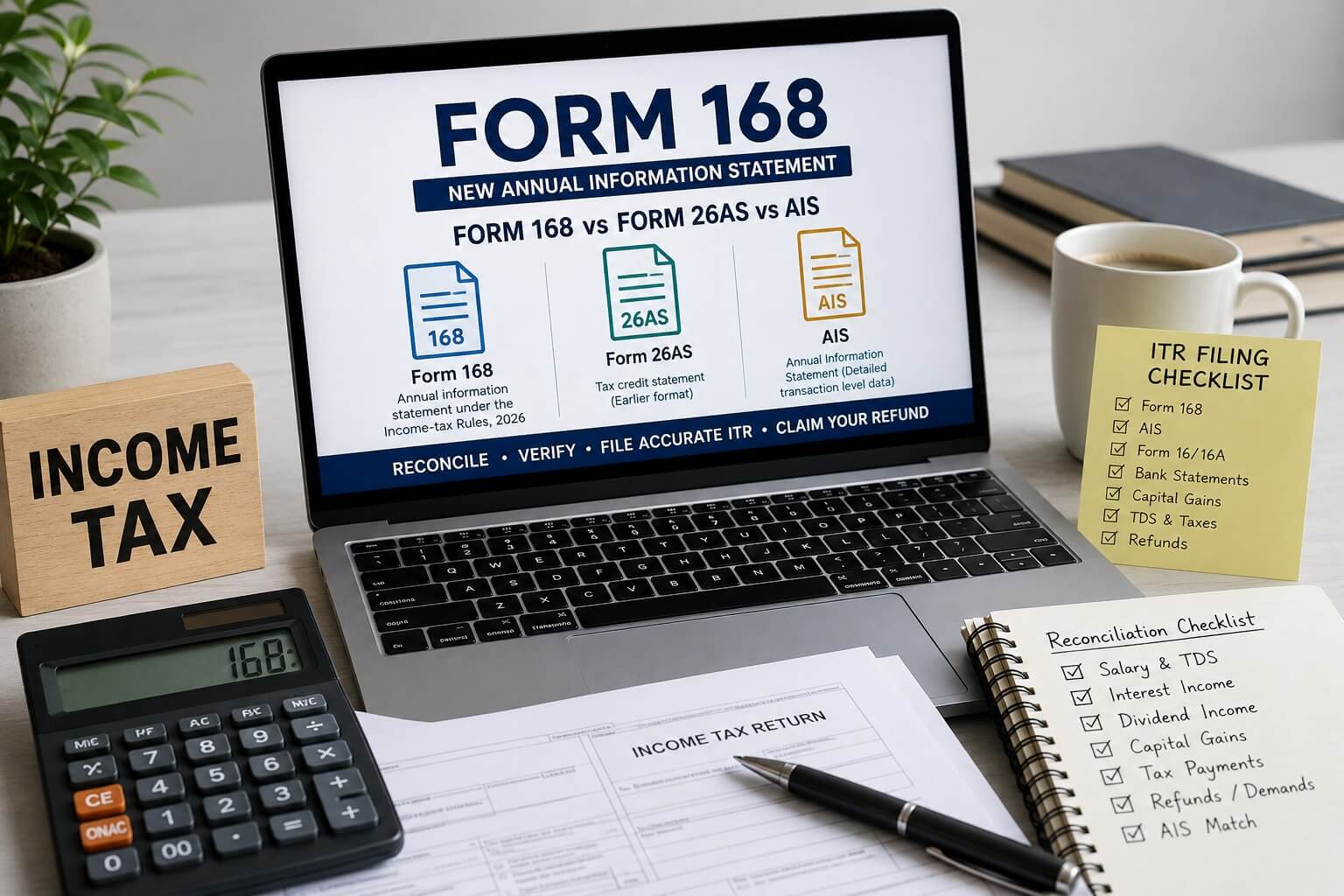

Before filing your return, reconcile your income with:

Many notices arise because returns do not reconcile with information already available to the Income Tax Department.

Every filing season, we see taxpayers making avoidable mistakes such as:

Professional review before filing can help prevent these issues.

At Dinesh Aarjav & Associates, NRI taxation is not just one of our practice areas—it is our core specialization.

We assist clients with:

With over 10 years of dedicated experience in NRI taxation, we help clients navigate complex cross-border tax issues with confidence while ensuring complete compliance.

For NRIs and Returning Indians, filing an Indian Income Tax Return is no longer just an annual compliance requirement—it is a critical part of managing your global tax affairs. Residential status, the correct ITR form, Foreign Tax Credit, RSU taxation, foreign retirement accounts, Schedule FA, Schedule FSI, and DTAA benefits all require careful evaluation.

At Dinesh Aarjav & Associates, we provide end-to-end Indian Income Tax Return Filing, Returning to India Advisory, Foreign Tax Credit planning, RSU and ESOP taxation support, and cross-border tax advisory tailored to your global financial profile.

Whether you are filing your first Indian return as an NRI, claiming a refund on a property sale, reporting foreign assets after returning to India, or navigating the tax treatment of RSUs and overseas retirement accounts, our team can help you file accurately, remain compliant, and optimise your tax position.

CA Disha Bansal is a tax professional at Dinesh Aarjav & Associates specializing in US taxation, India–US cross-border tax advisory, and NRI tax compliance. She advises individuals and NRIs on US tax return preparation, international reporting requirements, cross-border tax planning, and navigating complex India–US tax matters, helping clients manage their global tax obligations efficiently and compliantly.

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)