WhatsApp

WhatsApp

Call Us

Call Us

Email Us

Email Us

Whatsapp Community

Whatsapp Community

Would you like to schedule a call back

Planning to return to India from the USA, Canada, the UK, Australia, the UAE, Singapore, or another country? Before you book your tickets or ship your belongings, make sure you understand the tax, FEMA, banking, investment, and compliance implications of becoming an Indian resident again.

For every NRI, there comes a point when returning home becomes more than just an idea. Some return to be closer to family, others relocate for career opportunities, retirement, business expansion, or to provide their children with an Indian education.

Over the past decade, we have seen hundreds of returning NRIs make expensive mistakes—not because tax laws are overly complicated, but because they started planning after moving instead of before.

A simple decision such as delaying your return by a few weeks, restructuring overseas investments, or reviewing your retirement accounts before becoming an Indian resident can significantly affect your future tax liability.

Whether you are returning from the United States, Canada, the United Kingdom, Australia, the UAE, Singapore, or any other country, your move impacts much more than your residential address. It can affect:

Unfortunately, many NRIs discover these issues only after filing their first tax return in India or when they receive notices from banks asking them to update their residential status.

The good news is that most of these issues are completely avoidable with timely planning.

At Dinesh Aarjav & Associates, we have been advising NRIs and returning residents for over 25 years, helping clients across the USA, Canada, the UK, Australia, the UAE, Singapore, and several other countries navigate the tax, FEMA, and financial implications of relocating to India. Based on our experience, here are the 15 most common—and costly—mistakes every returning NRI should avoid.

This is, without question, the biggest mistake we see.

Many NRIs assume that tax planning can wait until after they arrive in India.

Unfortunately, by then, many planning opportunities may already be lost.

For example:

The best time to begin planning is 6–12 months before your intended move.

Early planning allows you to evaluate your global income, investments, retirement accounts, banking arrangements, and residency position in a coordinated manner rather than making decisions under time pressure.

Expert Tip: Returning to India is one of the few life events where the timing of your move can materially influence your tax position. Seeking professional returning to India consultancy before your relocation can help you plan effectively, as planning ahead often creates options that are no longer available after relocation.

One of the most common myths is:

"The day I land in India, I automatically become an Indian tax resident."

This is incorrect.

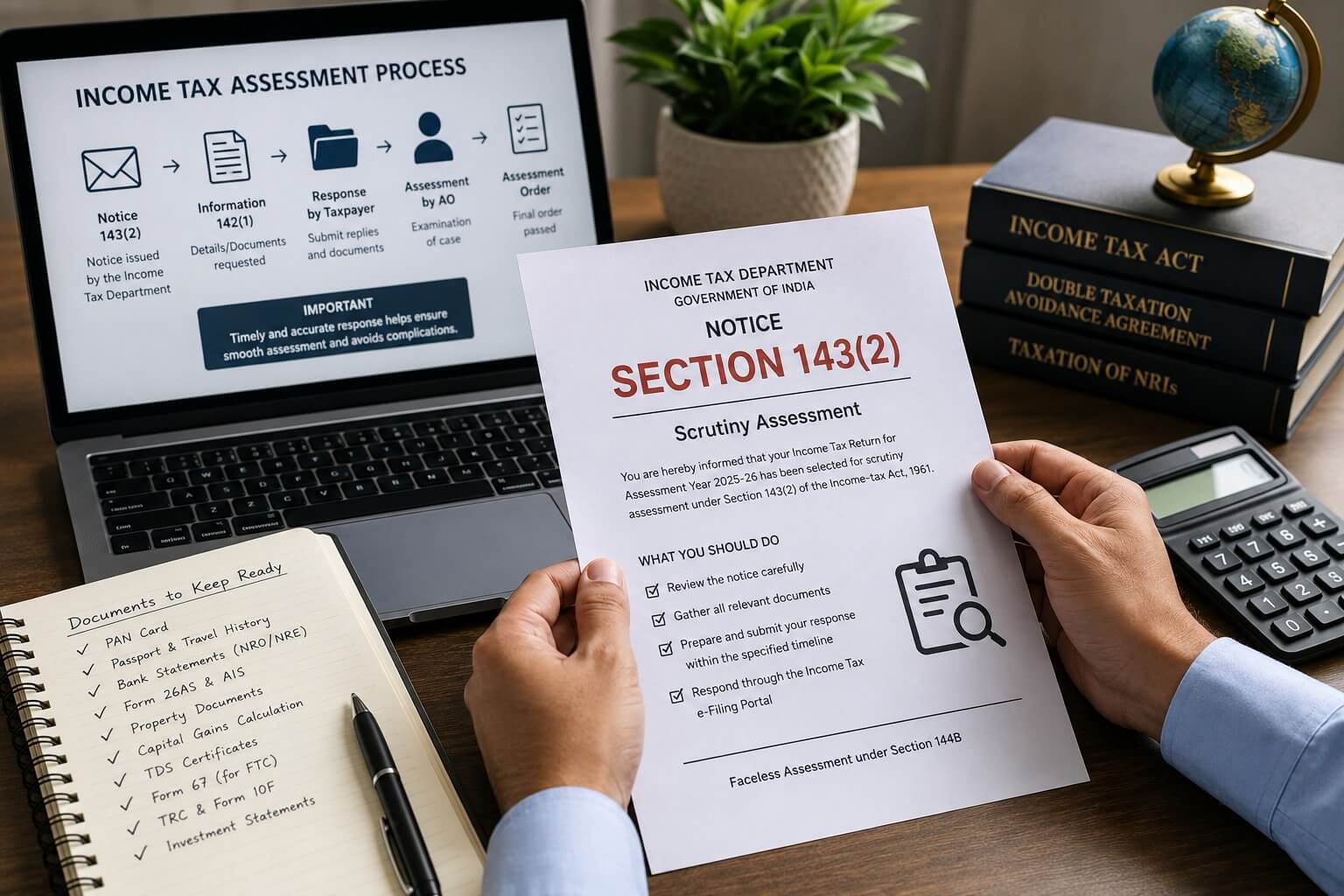

Under Indian tax law, your residential status depends on statutory conditions relating to your physical presence in India during the relevant financial year and preceding years.

Broadly, individuals may fall into one of three categories:

|

Residential Status |

General Tax Position |

|---|---|

|

Non-Resident (NR) |

Generally taxed in India on income received, accrued, or deemed to accrue in India. |

|

Resident but Not Ordinarily Resident (RNOR) |

Eligible individuals may receive beneficial treatment for certain foreign income during the transition period, subject to legal conditions. |

|

Resident and Ordinarily Resident (ROR) |

Generally taxable on worldwide income in India, subject to applicable treaty relief. |

Your residential status determines:

Getting this wrong can have long-term tax implications.

Among all the planning opportunities available to returning NRIs, RNOR (Resident but Not Ordinarily Resident) is perhaps the most valuable—and the most misunderstood.

Many professionals returning to India have heard of RNOR, but few understand how it can influence their tax planning without expert NRI Advisory.

RNOR is a transitional residential status available to eligible returning NRIs who satisfy the prescribed conditions under Indian tax law.

During this period, qualifying individuals may receive beneficial tax treatment for certain foreign income, providing valuable time to reorganize their financial affairs before becoming fully taxable on worldwide income as a Resident and Ordinarily Resident (ROR).

This transition period can be an ideal time to:

The opportunity is significant—but only if you plan before your status changes.

Many returning NRIs continue using their NRE account exactly as they did while living overseas.

However, your banking arrangements should be reviewed once your residential status changes under FEMA.

Your NRE account was designed for non-residents.

After becoming a resident under FEMA, you should notify your bank and discuss the appropriate redesignation process.

Similarly, your:

should also be reviewed.

Ignoring these requirements may create avoidable compliance issues later.

Ask ten returning NRIs whether they have heard about a Resident Foreign Currency (RFC) Account, and chances are that only a few will know what it is.

Yet, for many returning professionals, it can be one of the most useful banking tools available.

An RFC account allows eligible returning residents to continue holding foreign currency in India, subject to RBI regulations.

Depending on your financial profile, it may be particularly useful if you continue receiving:

Many returning NRIs automatically convert all foreign currency into Indian Rupees without consulting an NRI Tax Advisory expert to determine whether retaining foreign currency through an RFC account would better support their long-term financial goals.

One of the most expensive mistakes is selling overseas investments without considering how your relocation may affect taxation.

This applies to:

The tax outcome can differ depending on:

The same investment sold before your move and after your move can produce very different tax consequences.

Rather than making decisions based solely on market conditions, align your investment strategy with your cross-border tax position.

Professionals working for multinational companies often hold:

These forms of compensation frequently continue to vest after you relocate.

Without proper planning, this may result in:

If you expect future vesting events, review them before your move so that you understand the tax implications in both countries.

Another common misconception is:

"I'm moving back to India, so I should close all my retirement accounts."

In reality, withdrawing funds without a comprehensive tax review can be costly.

Returning NRIs may hold assets such as:

The taxation of these accounts depends on several factors, including the country of origin, the nature of the account, your residential status, and any applicable tax treaty.

Premature withdrawals may trigger tax liabilities or penalties in the country where the account is maintained and may also require careful consideration under Indian tax rules.

Instead of making hasty decisions, develop a coordinated withdrawal strategy that aligns with your long-term retirement and tax planning objectives.

One of the biggest misconceptions among NRIs is that once a Double Taxation Avoidance Agreement (DTAA) exists between India and their country of residence, they no longer need to worry about taxes.

Unfortunately, it isn't that simple.

A DTAA is designed to prevent the same income from being taxed twice, but it does not automatically exempt income from tax or remove your compliance obligations. You may still need to:

For example, a professional returning from the United States may continue receiving RSUs, dividends, consulting income, or pension distributions after relocating to India. Each type of income can have different tax implications depending on the applicable treaty and the individual's residential status.

Planning Tip: Don't assume that a DTAA will automatically protect you from double taxation. Proper reporting and timely claims are often just as important as the treaty itself.

Many returning NRIs focus exclusively on income tax and forget that the Foreign Exchange Management Act (FEMA) has its own set of rules.

Returning to India can affect how you hold:

In many cases, you may continue to hold overseas assets, but your residential status under FEMA changes how they should be managed.

The objective is not to close every overseas account immediately—it is to ensure your holdings remain compliant with the applicable regulations.

A coordinated review of your overseas assets before relocating can help avoid unnecessary compliance issues later.

Many NRIs decide to sell their Indian property after returning, assuming the process becomes easier once they are back in India.

However, property taxation can still involve several important considerations, including:

If the property is sold while you are transitioning between tax residences, careful planning can help you avoid unnecessary tax costs and compliance challenges.

Property transactions should ideally be reviewed before the sale is finalised rather than after the proceeds have been received.

One of the biggest changes after becoming an Indian tax resident is that your compliance obligations may expand.

Many returning NRIs continue to hold:

Depending on your residential status and the applicable reporting requirements, certain foreign assets may need to be disclosed in your Indian income tax return.

Incomplete or incorrect disclosures can create avoidable compliance issues in the future.

Keeping organised records of your overseas assets, acquisition dates, income, and supporting documentation can make future reporting significantly easier.

Your financial life may have been structured while you were living overseas.

You may have:

After returning to India, it is worth reviewing whether your estate plan still aligns with your current circumstances.

Cross-border succession planning is particularly important where assets are located in more than one country, as inheritance laws and administrative procedures can differ significantly.

A periodic review of your Will, nominations, and ownership structure can help ensure your family's wishes are carried out efficiently.

Many returning NRIs believe that once they move back, every overseas asset should be liquidated and every foreign bank balance should be transferred to India.

In reality, there is rarely a one-size-fits-all answer.

Before making large transfers, consider:

A phased remittance strategy is often more flexible than transferring everything at once.

Good planning considers not only today's requirements but also your long-term financial goals.

Returning to India today is far more complex than it was a decade ago.

A single relocation may involve:

Each of these areas can affect the others.

For example, the timing of your move may influence your residential status. Your residential status may affect how foreign income is taxed. That, in turn, can influence your Foreign Tax Credit claim and the reporting of overseas assets.

This is why successful return planning should be viewed as a financial roadmap, not a series of isolated decisions.

The earlier the planning begins, the greater the opportunity to preserve tax benefits, reduce compliance risks, and transition smoothly.

Before you relocate, make sure you have reviewed the following:

Returning to India is one of the few life events where decisions made before relocation can significantly influence future tax outcomes.

Whether you are moving from the USA, Canada, the UK, Australia, the UAE, Singapore, or another country, your relocation affects far more than your address.

It changes how your income is taxed, how your investments are managed, how your bank accounts operate, and how you comply with Indian regulations.

With the right planning, you can:

The key is to begin planning before your residential status changes.

Returning to India involves much more than filing an income tax return.

It requires coordinated advice across tax, FEMA, banking, investments, retirement planning, and international compliance.

At Dinesh Aarjav & Associates, we have over 25 years of experience advising NRIs and global families across the USA, Canada, the UK, Australia, the UAE, Singapore, and many other countries.

Our multidisciplinary team assists clients with:

If you are planning to return to India in the next 6 to 24 months, early planning can help you avoid costly mistakes and create a smooth financial transition.

Returning to India is more than a homecoming—it's a significant financial transition. The choices you make before your move can shape your tax efficiency, regulatory compliance, investment strategy, and long-term wealth.

By planning early, understanding your residential status, reviewing your global assets, and coordinating tax and FEMA implications, you can avoid common pitfalls and make your transition to India smoother and more financially secure.

Whether you're returning from the United States, Canada, the United Kingdom, Australia, the UAE, Singapore, or elsewhere, thoughtful planning today can help you protect your wealth tomorrow.

Returning to India is far more than a logistical move—it is a transition that affects your tax residency, banking arrangements, investment strategy, retirement planning, and regulatory compliance.

The decisions you make before relocating often have a greater financial impact than those made after you arrive.

By understanding these first eight common mistakes, you can begin your journey back to India with greater confidence and avoid many of the costly pitfalls that affect returning NRIs every year

CA Priyal Goel Jain is a Partner at Dinesh Aarjav & Associates and a leading expert in India–US cross-border taxation, NRI taxation, and international tax advisory. She advises NRIs, OCIs, and global families on complex cross-border transactions, tax planning, foreign asset reporting, and multi-jurisdictional compliance matters.

Stay in the loop, subscribe to our newsletter and unlock a world of exclusive updates, insights, and offers delivered straight to your inbox.

.webp)